If you had invested in Lululemon back in 2018 and held until today, your total return would’ve been close to zero. Add inflation and opportunity cost, and in real terms, it was even worse.

An investor who bought in September 2020 would also be sitting on a 50%+ loss today. And anyone who entered around December 2023, when the stock was in the $520s, would be down nearly 70%.

The market tends to overreact to short-term changes, and by short term, I mean a few quarters that create uncertainty. So this kind of swing doesn’t surprise me.

My job is to separate noise from fundamentals to understand what really changed, what didn’t, and whether there’s value left beneath the panic.

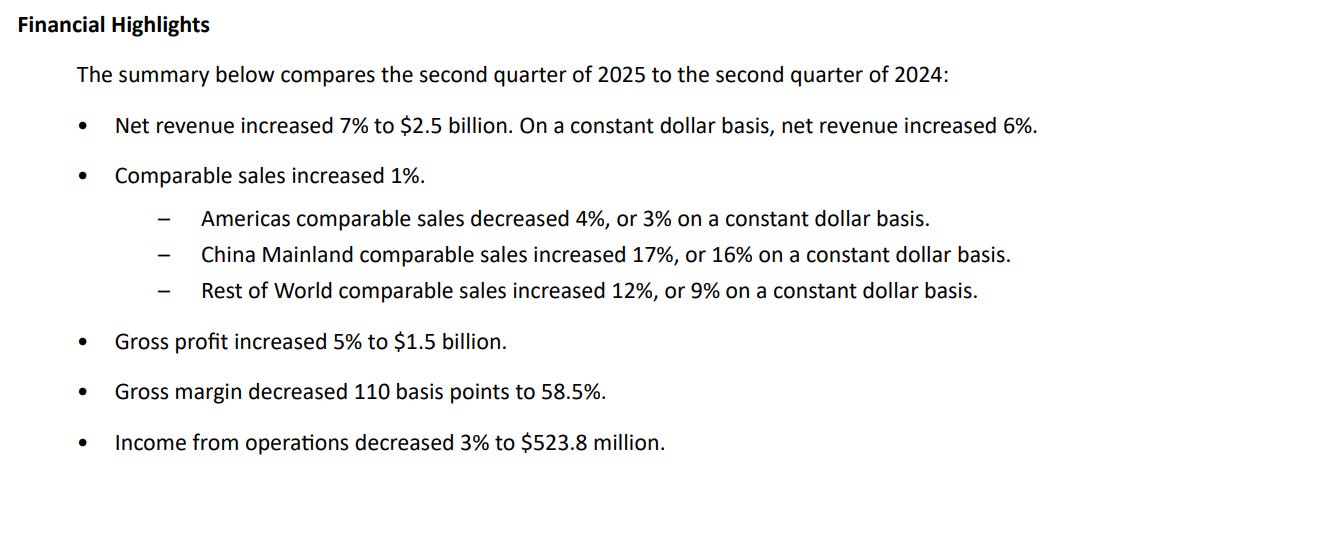

The recent decline comes down to slowing growth in North America, cut guidance, and rising competition. The headlines sound bad. But when you look beyond them, the business still stands strong — both financially and operationally.

Do we really understand what’s happening here — and why the stock is down?

When I say a stock is down, I’m really talking about the market’s perception of the company’s value, not just a price move on a screen.

But what actually makes a company’s value decline? It happens when earnings power weakens, the balance sheet deteriorates, the long-term outlook becomes riskier, or when the brand starts to lose relevance, innovation slows, competition tightens, and the moat erodes.

You could expand that list further, macro shifts (rates, spending cycles), operational mistakes (poor execution, inventory build-up), or capital decisions (buybacks at the wrong time, over expansion). But the core idea stays the same: the value falls only when something real and lasting changes beneath the surface.

So, do I see any of that here with Lululemon? Let’s look.

What I see is a premium global brand, with massive expansion potential in Europe and China, a strong balance sheet, cash in hand, and better margins than most of its peers — around 60% gross margins, a billion dollars in cash, and zero debt. The company is buying back shares, expanding internationally, and doing it profitably.

Then what’s the problem?

U.S. growth has slowed, consumers have become more selective, and management made a few mistakes: slower product refreshes, higher inventories, and some pricing missteps. The market punished those hard.

But those are fixable issues, not structural ones. The business underneath still looks strong.

A Split Story

If you’ve listened to the company’s recent earnings calls or gone through the filings, you’ll notice something interesting, it’s really two stories in one.

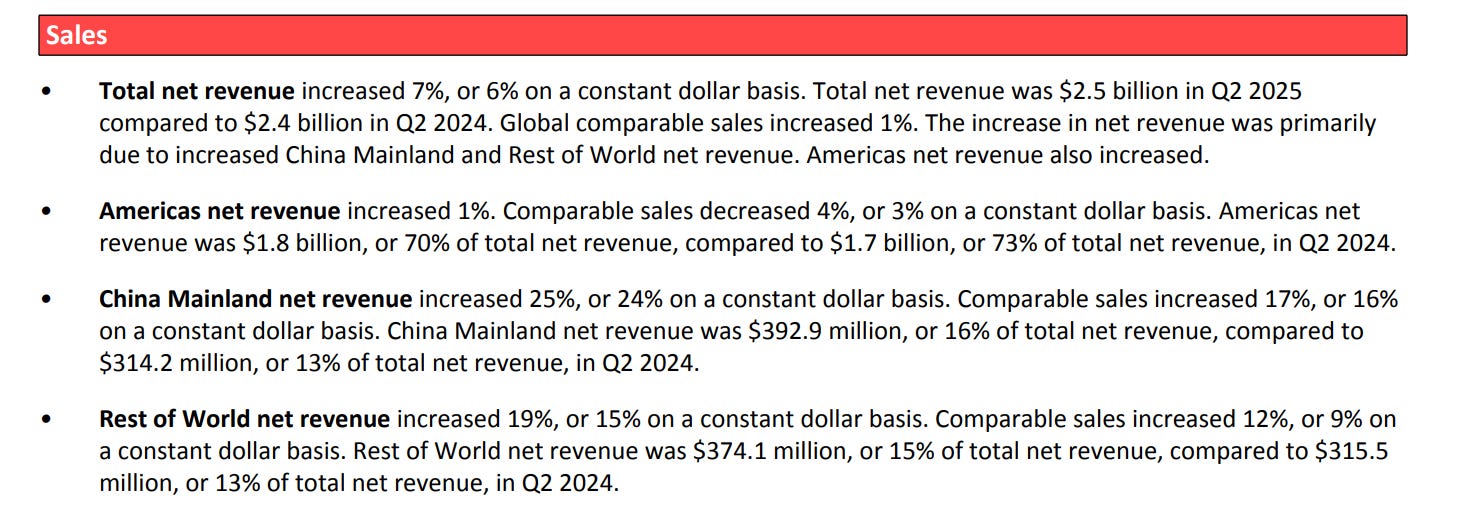

International growth is running in the mid-20s, while the Americas are soft. That’s the split. So the natural question is — why is the business growing strongly overseas but slowing at home? And why is that hitting the bottom line?

I’d say it’s a mix of things — tariffs, supply chain costs, inventory build-up, and a cut in guidance.

Each one on its own wouldn’t break the story, but together they’ve pressured margins and spooked investors who were expecting smoother execution.

The Americas are weak — consumers have turned cautious, and competition in premium activewear has intensified, especially as Nike and Adidas leaned heavily on discounts this year. Consumer sentiment has shifted too. The sense of newness just wasn’t there for Lululemon, traffic held up, but visitors didn’t quite feel the excitement of fresh products.

International markets are strong, China and Europe both delivered double-digit growth, expanding quickly in regions that are still far from saturation. The brand remains unknown to many potential future loyal customers, which makes this a genuinely exciting story, if it’s executed well.

That global diversification is exactly what gives Lululemon its resilience. When one region slows, others pick up the pace.

Think of Coca-Cola, Nike, or Apple, brands that travel effortlessly across borders, cultures, and lifestyles. There’s something special about that. Most products can’t even scale smoothly between U.S. states, let alone countries.

Lululemon has that rare potential, the ability to become a truly global lifestyle brand, not just a retailer. That’s a powerful advantage over time.

The company has now reached nearly 800 stores globally, with new openings supported by solid demand and strong unit economics. This is profitable growth, not expansion for the sake of expansion.

Even as the company grows rapidly internationally, its margins remain among the best in retail. Yes, they’ve dipped slightly because of tariffs and higher costs, but at around 58%, they’re still well above peers like Nike and Adidas.

That kind of margin strength says a lot, it means the brand still commands pricing power, and more importantly, it still has the trust and loyalty of its customers.