Value investing is not just about a low P/E ratio.

Return on Capital matters more than the price you pay.

After many years of investing, I wanted to share my view on how a low P/E ratio can trick us into actually paying more. Like everything else, investing is changing, and buying “cheap” stocks doesn’t work the way it used to.

To succeed today, quantitative analysis based on low P/E ratios is not enough. It requires business understanding, a focus on Return on Capital, and patience for the long term. At least, this is my everyday task now.

Compounding is an important concept in investing, and it is actually quite simple to imagine.

If I am the owner of 10% of a company that earns $100 million per year, I still own the same 10% the next year, but the company earns more. The year after, it earns even more. My percentage ownership stays the same, but the earnings themselves keep getting bigger.

This is a Compounding Machine, though finding one is the hard part. The big question for an investor is: If you find such a company today, how much should you pay for those future earnings?

To answer that, we have to look at Return on Capital.

The Two Types of Businesses

There are really only two types of companies: those with high returns on capital and those without.

High-Return Business: Puts a dollar to work and creates 15 to 20 cents (or more) of new value.

Low-Return Business: Puts a dollar to work and struggles to create 10 cents.

Over time, the high-return business creates tremendous wealth, while the low-return business just treads water.

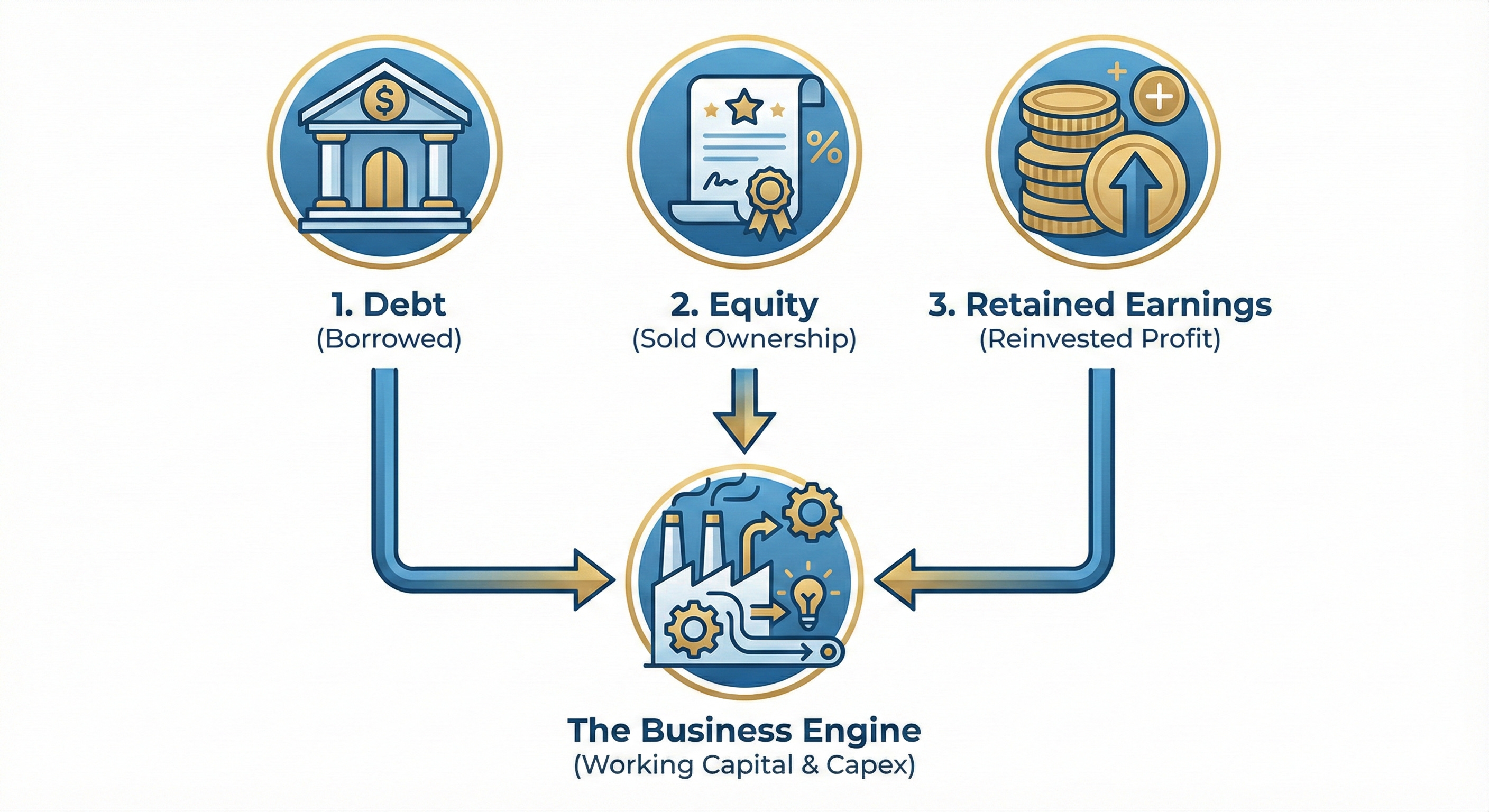

What Is Capital?

Capital is just the fuel the business needs to operate. It comes basically in three forms:

Equity: Selling a piece of ownership.

Debt: Borrowing money

Retained Earnings

Companies use this capital for Working Capital (day-to-day bills) and Capex (machinery and buildings).

Ideally, I want to own a company that doesn’t need to constantly raise outside capital.

Measuring Efficiency: Return on Capital Employed (ROCE)

I calculate return on capital simply. I want to know how much profit the business generates relative to the cash and assets tied up in it.

The formula I use is:

ROCE = EBIT ÷ (Equity + Debt - Cash)

Note: I subtract cash because idle cash isn’t “working.” I use EBIT here to see the pure operating power of the machine, but I never ignore interest expense when calculating the final valuation.

How Do Companies Grow?

To increase earnings, a company can invest in new factories, research, or buy other companies. They fund this through Retained Earnings (the net income they don’t pay out as dividends).

But, not all growth is good growth. If a company spends $1 to earn 5 cents, they are destroying value. We want companies that spend $1 to earn 20 cents.

Let me show you the math behind why a “High Return” company is worth paying up for.

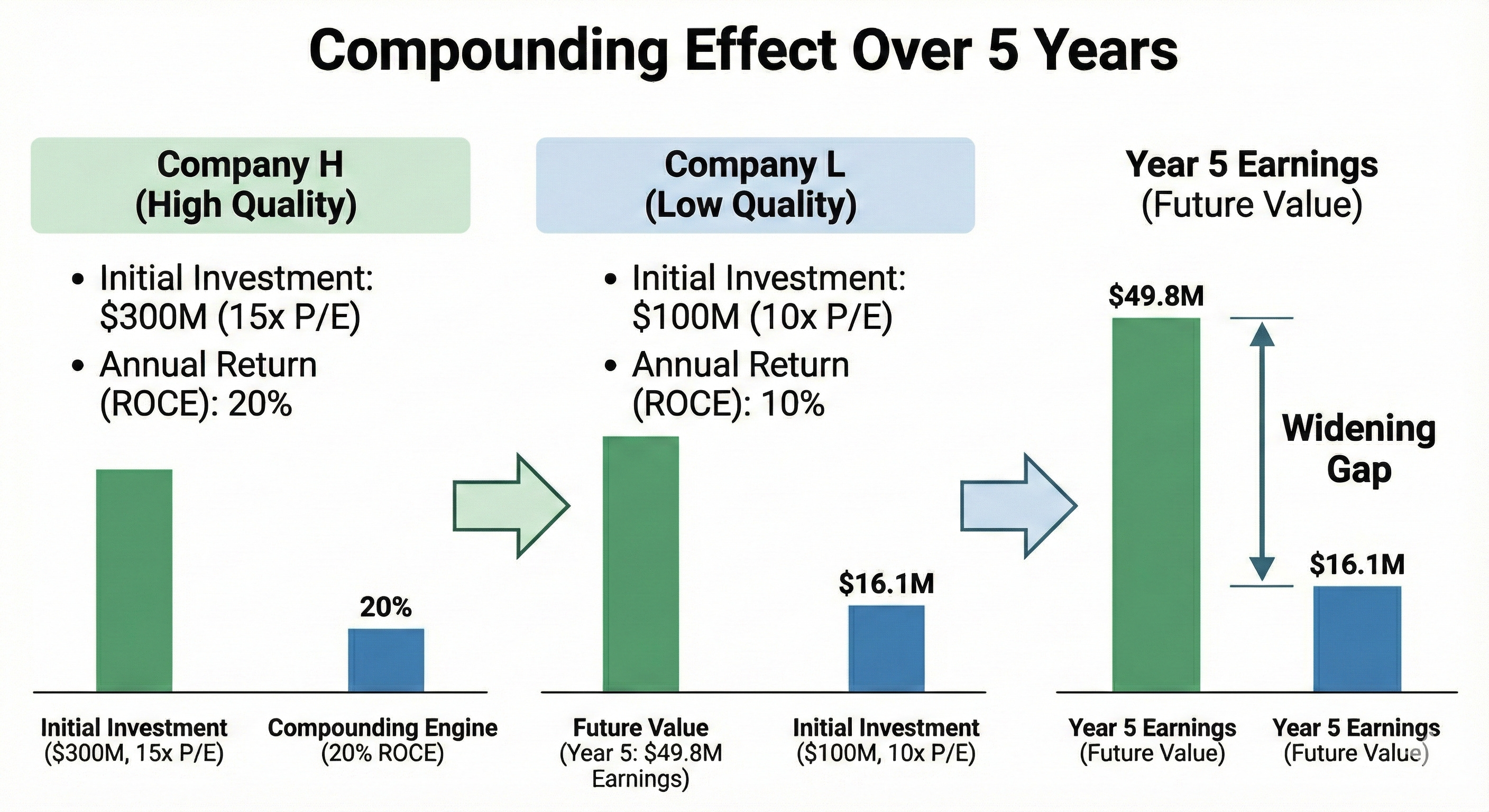

Scenario 1: The “Expensive” High Quality vs. The “Cheap” Low Quality

Imagine two companies. Both have $100M of Capital Employed and they reinvest all their profits back into the business.

Company H (High Quality)

20% Return on Capital.

It looks “expensive” trading at 15x Earnings.

Price you pay: $300 Million.

Company L (Low Quality)

10% Return on Capital.

It looks “cheap” trading at 10x Earnings.

Price you pay: $100 Million.

Most value investors buy Company L because of the low P/E. But look at what happens over 5 years.

The Starting Line (Year 0)

Company H: Earns $20M

Company L: Earns $10M

The Finish Line (Year 5)

Company H: Now earns $49.8M

Company L: Now earns $16.1M

The Reality Check: Even though you paid a high price for Company H ($300M), because the earnings grew so fast, you are now effectively paying just 6x its current earnings.

Meanwhile, for Company L, you are paying 6.2x its earnings.

Even though Company H was 50% more expensive to start with, it became the cheaper stock in just 5 years because of how fast it compounded. If you focus only on a low starting P/E, you miss the magic.

The longer you hold, the more value H will create.

Scenario 2: The True Fair Fight

Now, let’s make the starting point identical. Imagine you have $100 Million to invest. You find two companies that both earn $10 Million a year (so both trade at a P/E of 10x).

Company H2

Price you pay: $100M

Year 0 Earnings: $10M

ROCE: 20% (This company grows earnings at 20% per year).

Company L2

Price you pay: $100M

Year 0 Earnings: $10M

ROCE: 10% (This company grows earnings at 10% per year).

Fast Forward 5 Years:

Company H2: The earnings have compounded to $24.9M.

Based on your $100M investment, you are now earning a 25% yield (or a P/E of 4x).

Company L2: The earnings have compounded to $16.1M.

Based on your $100M investment, you are earning a 16% yield (or a P/E of 6.2x).

The Result: Even though you paid the exact same price for the exact same earnings on Day 1, the “High Return” machine pulled ahead massively. The longer you hold, the wider this gap gets.

Final Thoughts

Just because a stock looks cheap doesn’t mean it’s a good investment.

There are many investors who bought Apple between 2012 and 2016 when it was trading like a value stock. But they sold as soon as it reached their “estimated value.”

2011-2017: Apple compounded at roughly 14%.

2017-2024: Apple compounded at 30%+.

Those who sold early missed the best years of the compounding machine. As Charlie Munger always said, “The first rule of compounding is to never interrupt it unnecessarily.”

Find the high-return businesses, pay a fair price, and let them do the work.