2026 has started with more geopolitical noise than where we left 2025.

As I write this, markets are taking the headlines badly.

But this is exactly when you pay attention. The best chances are rare. They don’t show up often. When they do, you need to be ready.

Charlie Munger said opportunities come to a prepared mind. That’s the point: you do the work early.

Investing is mostly study, not action. Most of the time, the right move is to do nothing.

Right now, many good companies still look expensive. The prices leave no room for mistakes. So I’m building my watchlist, deciding what I’m willing to pay, and then waiting.

In late 2025, I shared Watchlist #1.

5 Quality Stocks I’m Watching

In investing, everything starts with opportunity cost. I am constantly comparing my best idea against the next best alternative.

Here are 5 more businesses I’m watching, and the prices I’m waiting for in 2026

What they all have in common:

High Switching Costs — once you’re in, it’s hard to leave. These businesses become part of how customers operate.

Disconnected Narratives — the story around them is worse than the reality. Headlines and sentiment are driving the price more than the actual business performance.

Real Free Cash Flow — they generate cash after paying for what the business needs. That gives them options: reinvest, buy back shares, or strengthen the balance sheet.

A Moat I Trust — I believe they have real protection around the business. Something that makes it hard for competitors to take customers and profits.

All five are currently hated or ignored for reasons that are likely temporary or exaggerated.

And because sentiment has already pushed them closer to what I think is fair value, I’m watching these names more closely than the rest, to see if the price drops to where I’d actually want to buy.

My prices might surprise you. But my job isn’t to be optimistic. It’s to avoid big mistakes. I want a price that gives me breathing room.

That’s what a margin of safety is.

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier

1. HubSpot (HUBS)

Current Price: $311 Market Cap: $16.3B

The business is solid. They generate roughly $3 billion in revenue and are free cash flow positive. Growth is steady at around 15%.

The Problem: The stock price is priced for 25%+ growth forever. At $329, the math doesn’t work. If AI slows their seat expansion or margins compress even slightly, this stock has a long way to fall.

The Price I’m Waiting For: $215 – $235 I want a margin of safety. If the price drops to this range, the risk/reward flips in my favor. Until then, I’m not interested.

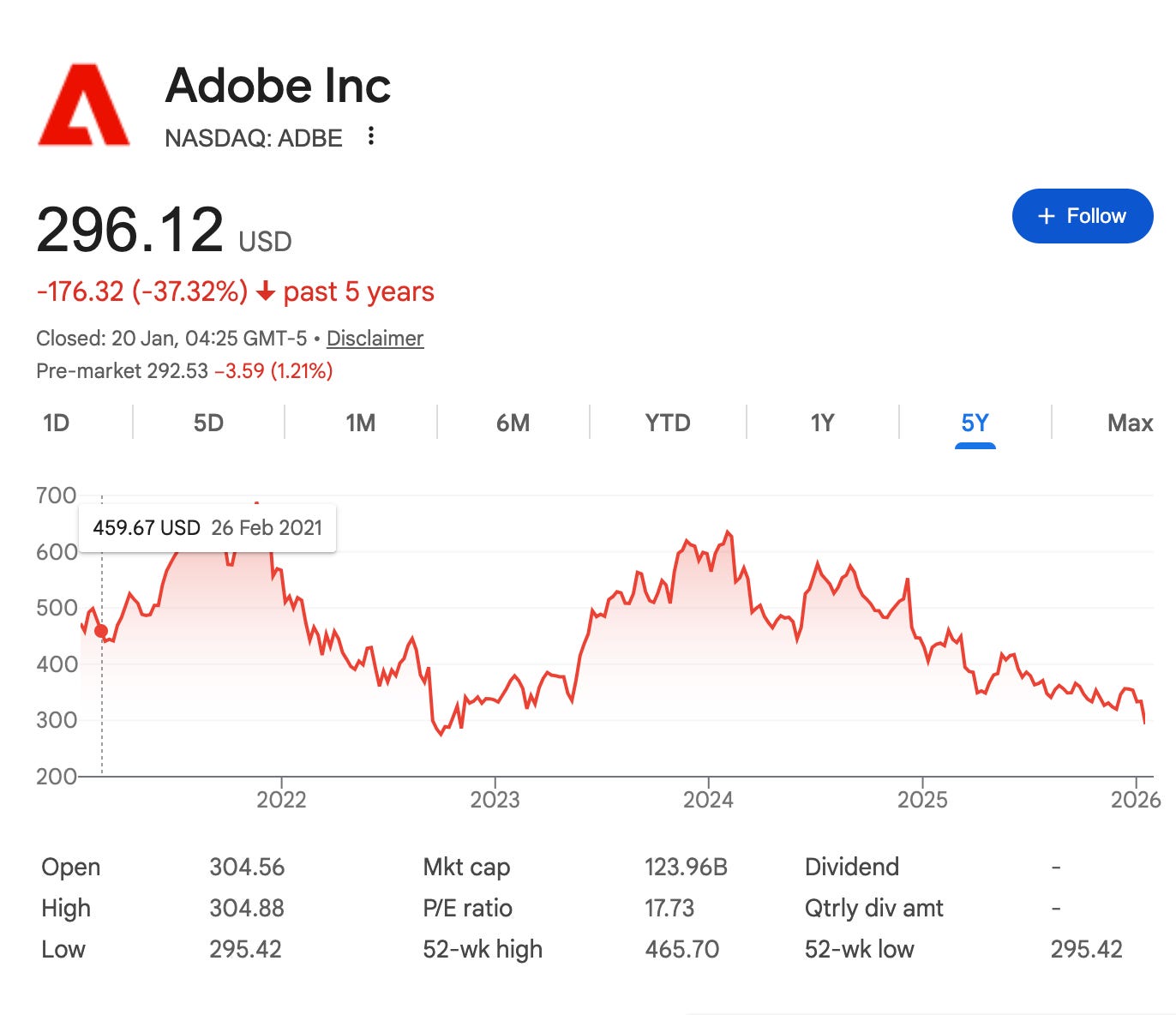

2. Adobe (ADBE)

Current Price: ~$296 Market Cap: ~$124B

Adobe stock is “dead money” right now. It’s trading near $296 because the market is convinced AI will kill their business.

I disagree. Corporate workflows are built on Adobe. Switching costs are high, and compliance is messy. The financials tell a different story than the narrative: Adobe generates $23.8 billion in revenue and a massive $8.9 billion in Free Cash Flow.

The Price I’m Waiting For: $243 I am looking for a further 18-20% discount. At $243, you pay just 10x Free Cash Flow. That prices the company for zero growth. If they grow at all, you win.

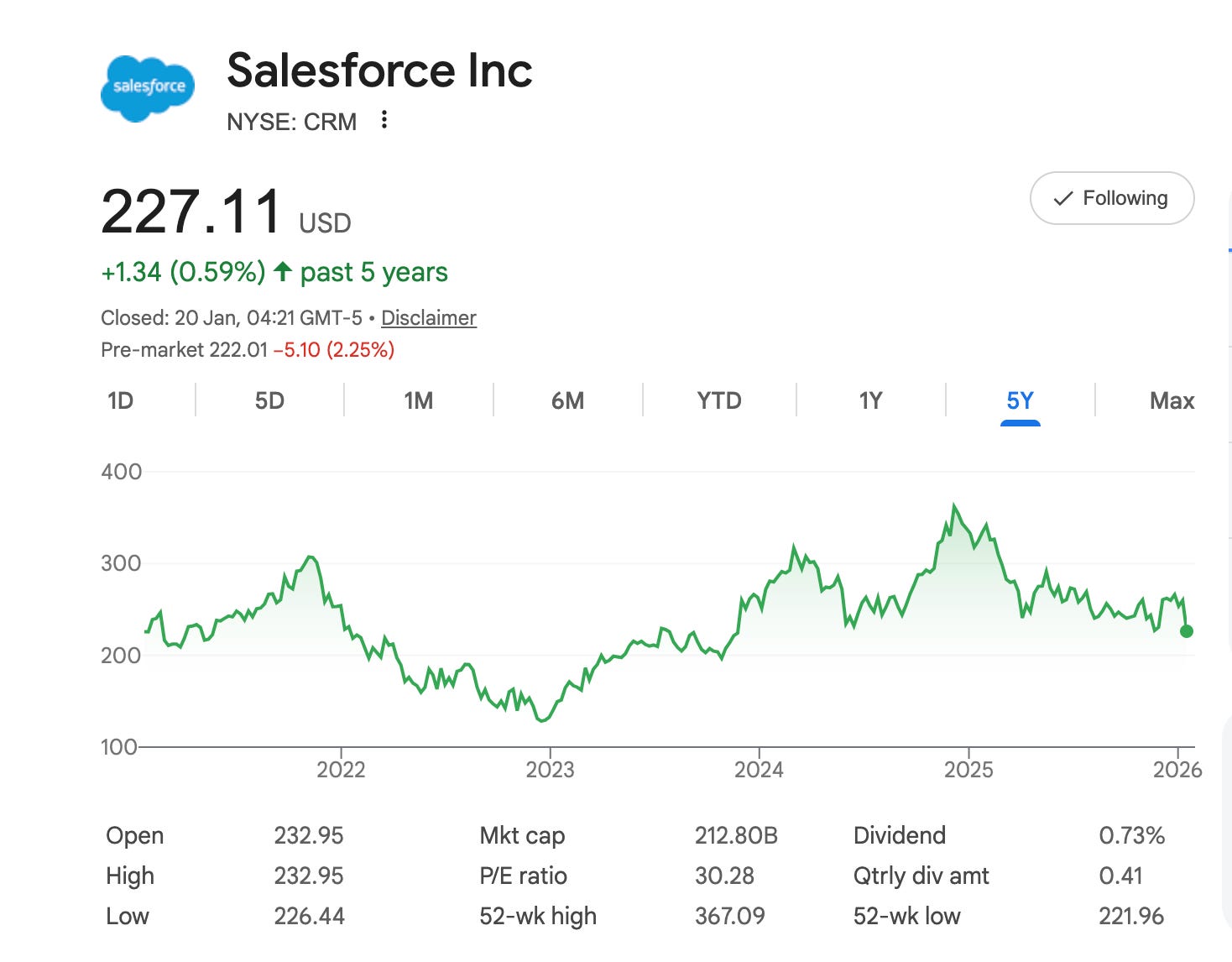

3. Salesforce (CRM)

Current Price: ~$227 Market Cap: ~$212B

Salesforce is down significantly, trading around $227. The business is a cash machine, pulling in $40 billion in revenue and over $12 billion in Free Cash Flow. But even at this lower price, it’s not a screamimg buy yet.

The Price I’m Waiting For: $175 At $175, you would be buying a software monopoly for roughly 14x Free Cash Flow. That is a bargain for a company with this level of customer retention.

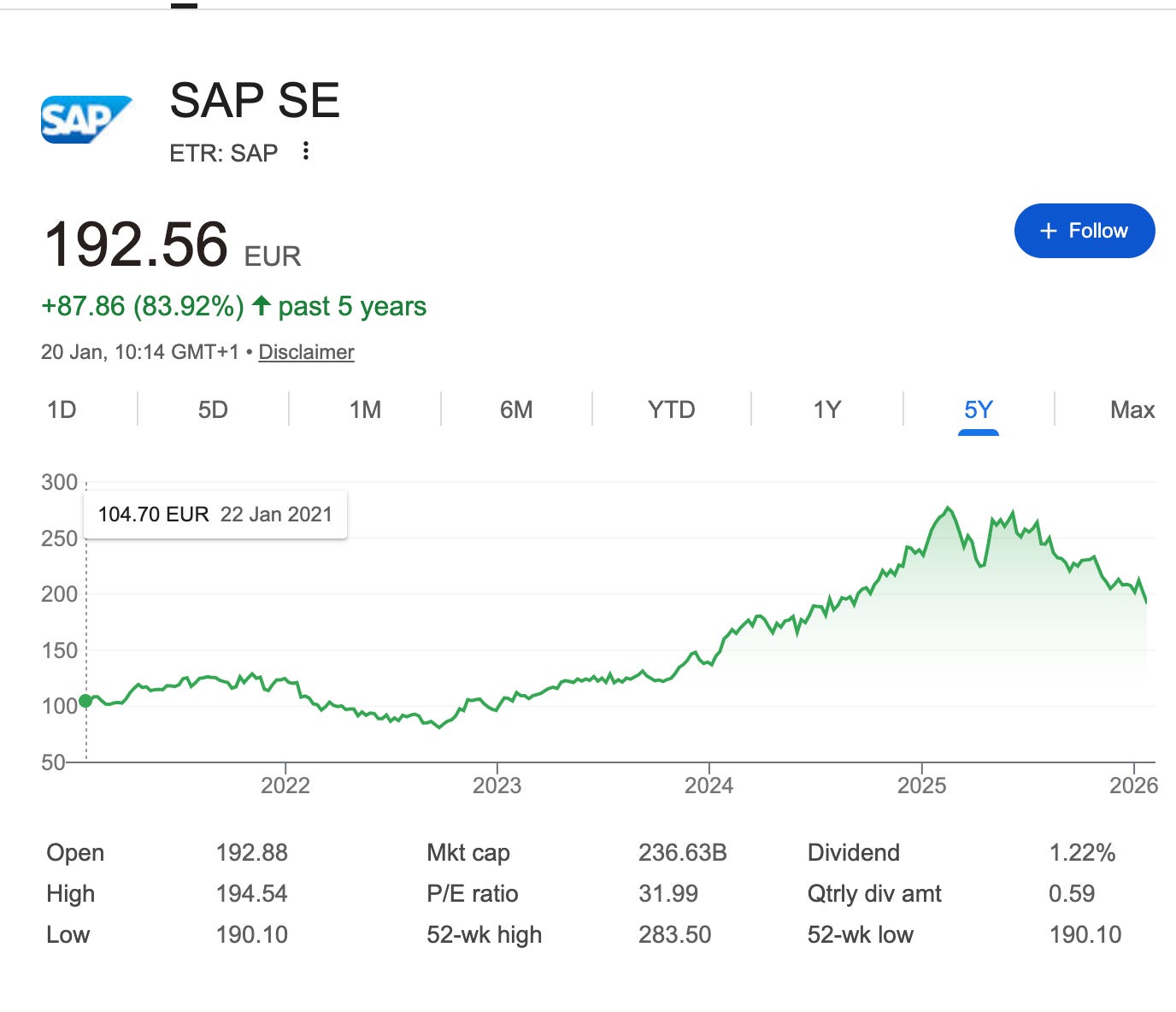

4. SAP (SAP)

Current Price: ~$233 Market Cap: ~$287B

SAP has a premium valuation because investors treat its cloud backlog as a safety net. Revenue is steady at $40 billion, but you are paying nearly 33x Free Cash Flow for that safety.

The Price I’m Waiting For: $116 To get interested, I need the price to be cut in half. At $116, you pay roughly 16x FCF. This treats SAP like the utility company it is, rather than a high-growth cloud stock. I want to pay for the cash, not the hype.

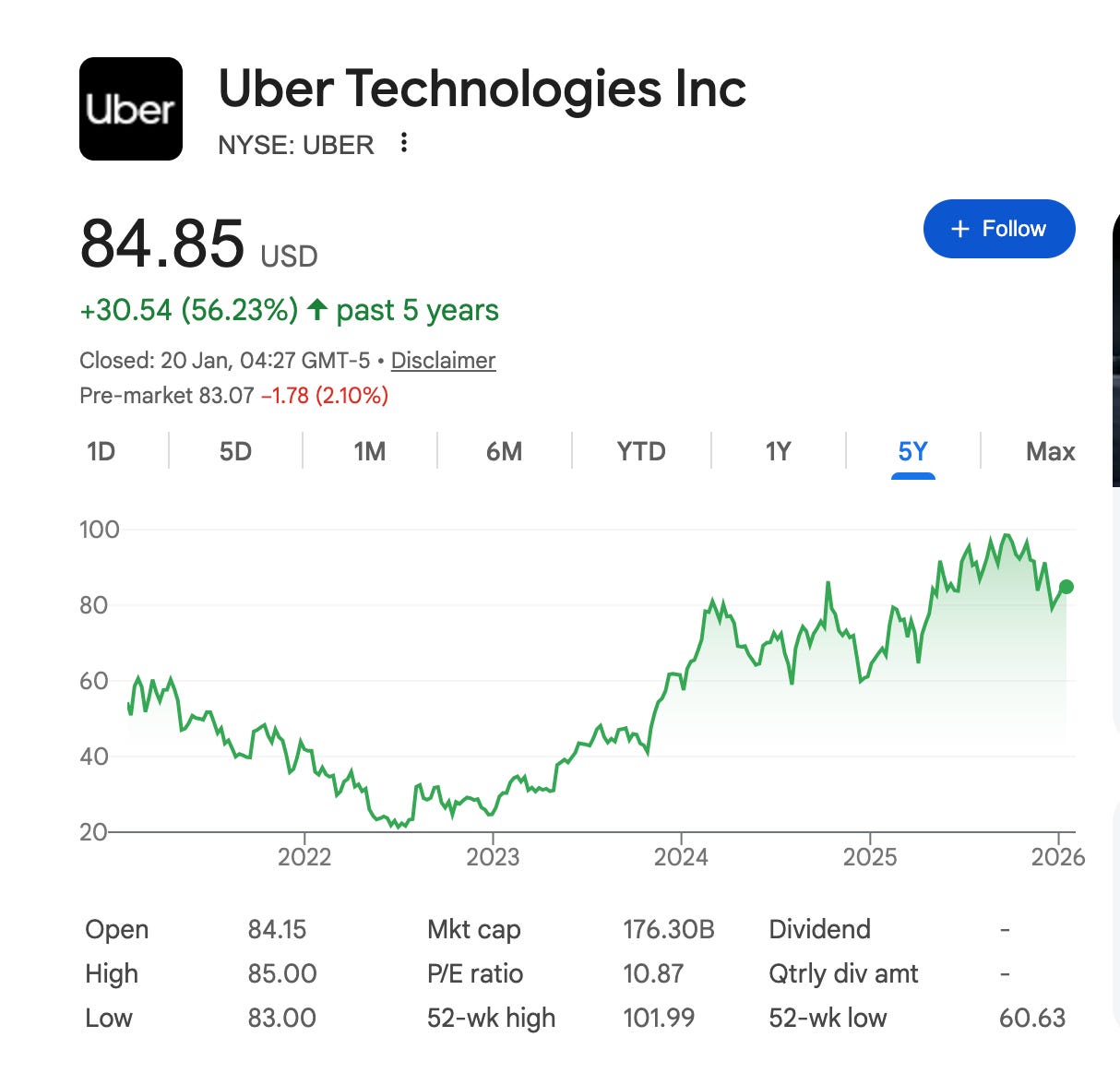

5. Uber (UBER)

Current Price: ~$85 Market Cap: ~$176B

Uber has successfully pivoted. They are generating $49.6 billion in revenue and $8.7 billion in Free Cash Flow. The market currently pays about 20x FCF for this.

The Price I’m Waiting For: $55 I want to pay 12–14x Free Cash Flow. At $55, you are buying a global logistics network for the same multiple as a boring industrial stock. If the economy slows, this entry price protects you.

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier