What do they actually do?

The Trade Desk as a marketplace where brands buy ads across the internet.

Old world: Ford wanted TV ads → call a network → negotiate → slow, inefficient.

New world: Ford’s agency logs into TTD, uploads the ad, picks the audience (“men 25–40 who like trucks”), and presses go.

Within milliseconds, TTD’s system bids on ad slots across:

Connected TV (Disney+, Hulu, etc.)

Spotify, podcasts

Websites (NYT, ESPN, etc.)

What they don’t do: they don’t buy ads inside Google Search or Meta (Facebook/Instagram). Those are closed ecosystems where outsiders can’t bid freely.

They take a small fee on every ad dollar that flows through their platform.

The moat

Google both owns a lot of the ad inventory (like YouTube) and runs one of the tools used to buy ads. That’s like the referee also owning one of the teams. Even if they try to be fair, the incentives are messy.

TTD is different:

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier

They own zero media

They don’t own TV channels, websites, or ad space

They’re just the buying tool

So big brands trust them more to spend money where it actually works, not where the platform owner wants it to go.

They’ve kept over 95% of customers every year for 11 years. Once agencies train on TTD, they rarely switch.

The “real” profits (GAAP)

The stock compensation

TTD pays employees a lot in stock. That cost shows up in GAAP earnings, and it matters because it dilutes shareholders over time.

In the first 9 months of 2025:

Stock paid to employees: $378m

GAAP profit: $256m

“Adjusted” profit (Wall Street’s version): $589m

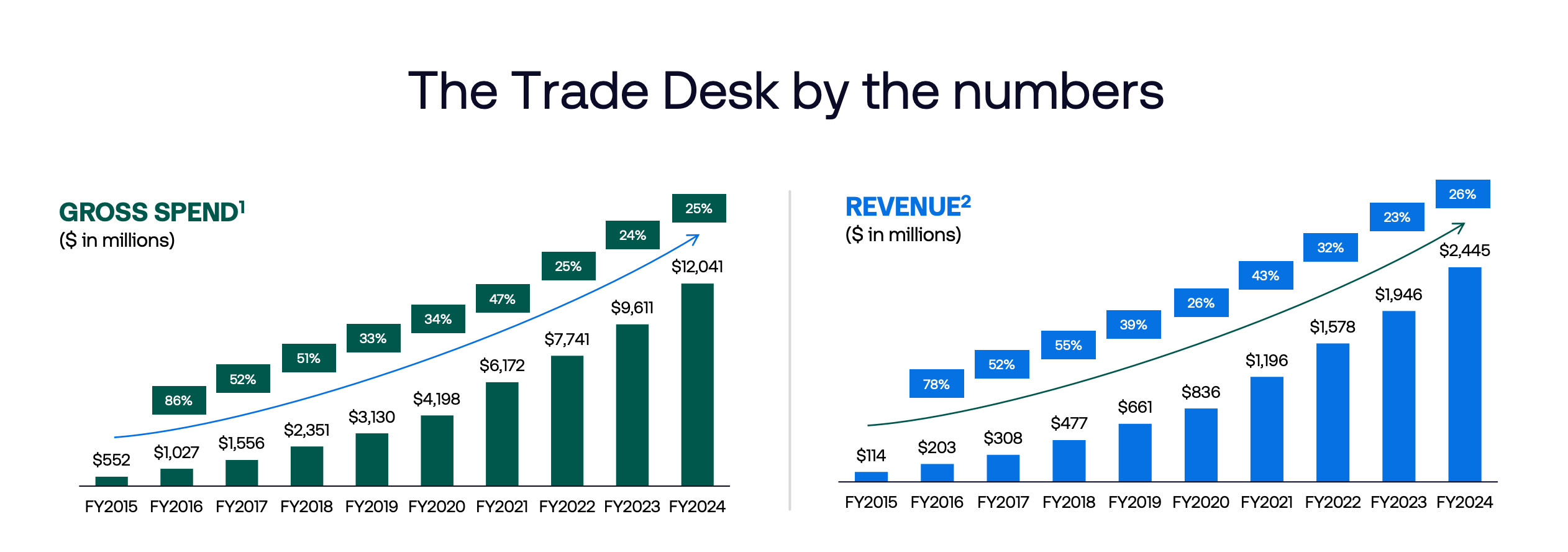

Why growth is slowing

Growth used to be 40%+. Now it’s more like low-20s.

Main reasons:

Bigger base: it’s harder to grow 40% when you’re already doing $2.5B revenue.

Market maturing: digital advertising isn’t “new” anymore.

Management’s Q4 2025 guide implies roughly 18–20% growth (excluding political ads), which is likely the new normal.

1) It’s harder at this size

40% growth on $500m is easy math. 40% on $2.5b means finding about $1b of new revenue every year. That’s a huge ask, even for a best-in-class platform.

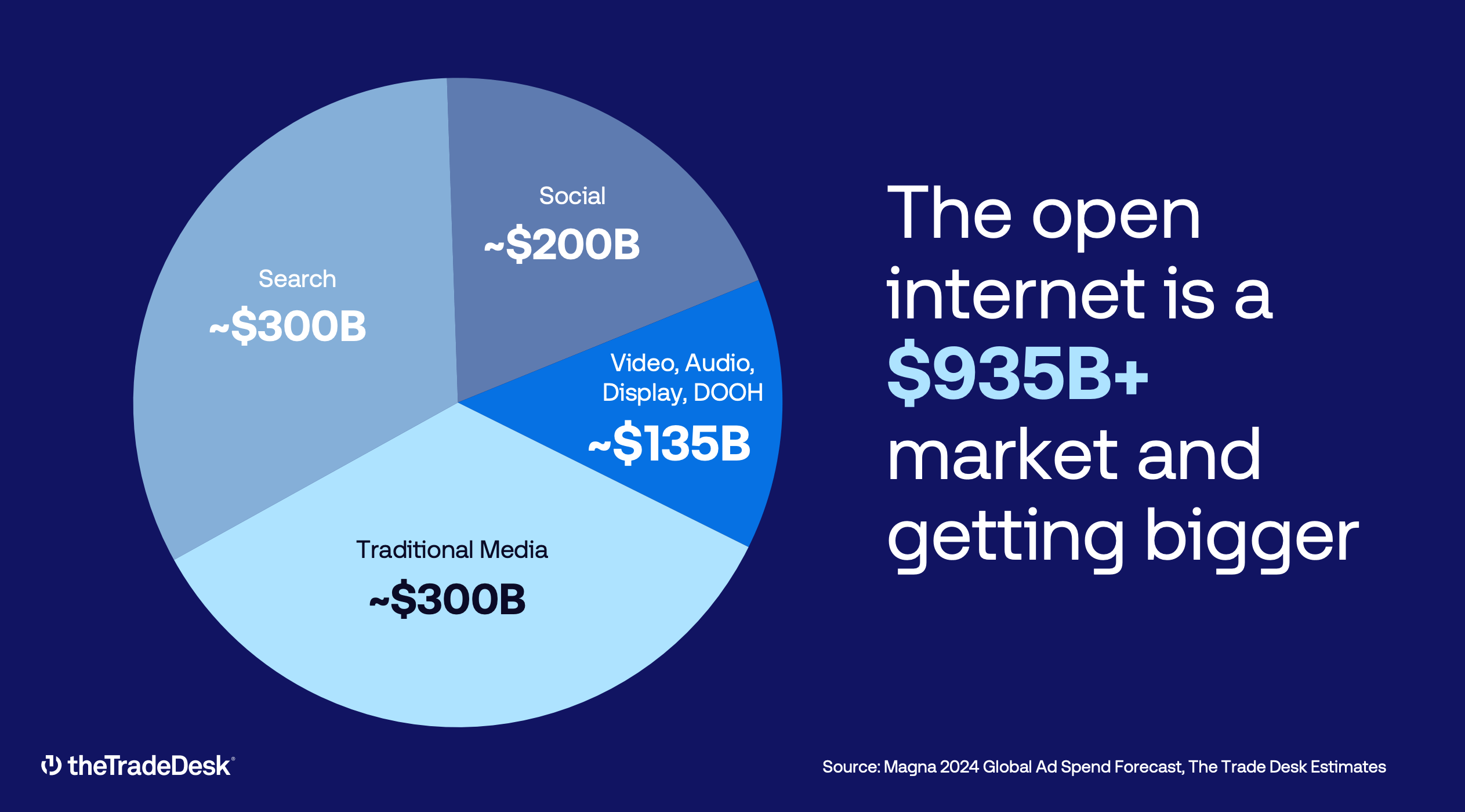

2) The market is maturing

Digital ads aren’t a fresh “land grab” anymore. Growth now comes more from taking share (from other platforms or old TV budgets) than from a wave of new adoption.

3) Amazon changed the game in CTV

Amazon is moving aggressively into premium streaming inventory and often makes buyers use Amazon’s own tools to access it. That locks TTD out of part of the best inventory, which limits how fast budgets can shift onto TTD.

The long-term growth range: 15% to 20%

If you’re underwriting the next 5 years, don’t anchor to the 40% era. This looks more like a steady “compounder” profile.

2026: roughly 16%–20% revenue growth

2027–2030: a gradual fade toward 14% as the company gets larger.

What keeps growth above 15%?

Management’s main levers are:

1) International

They’re still heavily US-weighted. If they truly crack Europe and Asia, that’s meaningful runway.

2) Retail media / shopper marketing

Partnering with retailers and using purchase data to target and measure results is a big growth pocket, because it ties ads to actual sales.

3) Connected TV

As cable declines, ad budgets keep moving to streaming. Programmatic buying is a natural fit here, and TTD is one of the key pipes.

What holds it back?

1) US saturation

They’re already big in the US. It’s hard to double when you’re already in almost every major agency relationship.

2) The Amazon wall

If Amazon keeps premium inventory increasingly “closed,” that’s a real ceiling on how much of the best CTV spend TTD can touch.

Valuation: where to feel comfortable

Once you accept 15%–20% as the likely long-run growth range, the price you pay matters a lot.

Scenario A: $35/share

You’re paying roughly 40x “real” earnings for 15–20% growth.

Scenario B: $25/share (your $12B–$13B market cap zone)

You’re closer to 27x real earnings.

Bottom line

The hyper-growth phase is likely over. This is becoming a high-quality compounder.

Your $12B–$13B market cap target is a sensible entry point for this phase of the business, because it matches the slower (but still strong) growth reality and gives you margin of safety.

5) My comfort-zone price

At about $35/share:

Market cap $17.2B

Real P/E 39x (not cheap)

At my target $12–13B market cap:

Share price roughly $24.50–$25

Real P/E around 27x

27x GAAP earnings for a company growing 20% with a real moat and 95% retention is reasonable.

At 39x, you’re paying extra for perfection, basically betting growth re-accelerates (AI, international, etc.).

My take

The good: best product in its niche, trusted “neutral” platform, insanely sticky customers.

The bad: heavy stock pay means your real earnings are lower and you get diluted. Growth has normalised to 20%.

I want margin of safety, wait for $25. At $35, it’s a great company, but the price is a bit stretched.

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier