Hong Kong-listed Chinese internet stocks became very popular from around 2008 until 2020. The reason was not hard to understand. China had a large population, a younger digital consumer base, and the digital economy was solving real problems in daily life.

E-commerce, social media, digital payments, delivery, games, and online services were not just nice things to have. In many places, they helped solve problems where infrastructure was still catching up.

That created a big tailwind for companies like Alibaba ($BABA), Tencent ($TCEHY) , Baidu ($BIDU), JD.com ($JD), Meituan (3690.HK), and NetEase ($NTES).

For a long time, these companies were growing revenue, entering new markets, and becoming more important in everyday life, so the market was willing to pay for that growth.

After 2020, the story changed. Regulation became more important, the internet crackdown hurt investor confidence, consumer behaviour changed, and the macro economy in China became harder. The property market also became a major pressure point. Property activity fell sharply: real estate development investment fell from RMB14.1 trillion in 2020 to RMB8.3 trillion in 2025, while commercial housing sales value fell from RMB17.4 trillion to RMB8.4 trillion.

That changed the background for Chinese consumer and internet companies.

This is not only a company-specific story. It is part of a wider reset in how investors think about Chinese internet companies.

Tencent’s market cap at HKD4.298 trillion, which is about US$550 billion. Alibaba is more famous in the West because of Jack Ma and because e-commerce is easier to explain. Tencent is less familiar, but I think it is the more interesting business to study because it touches so many parts of digital life in China.

Business Quality

Tencent is not only a gaming company. It owns several different businesses: domestic games, international games, social networks, marketing services, FinTech, business services, cloud, and Weixin/WeChat.

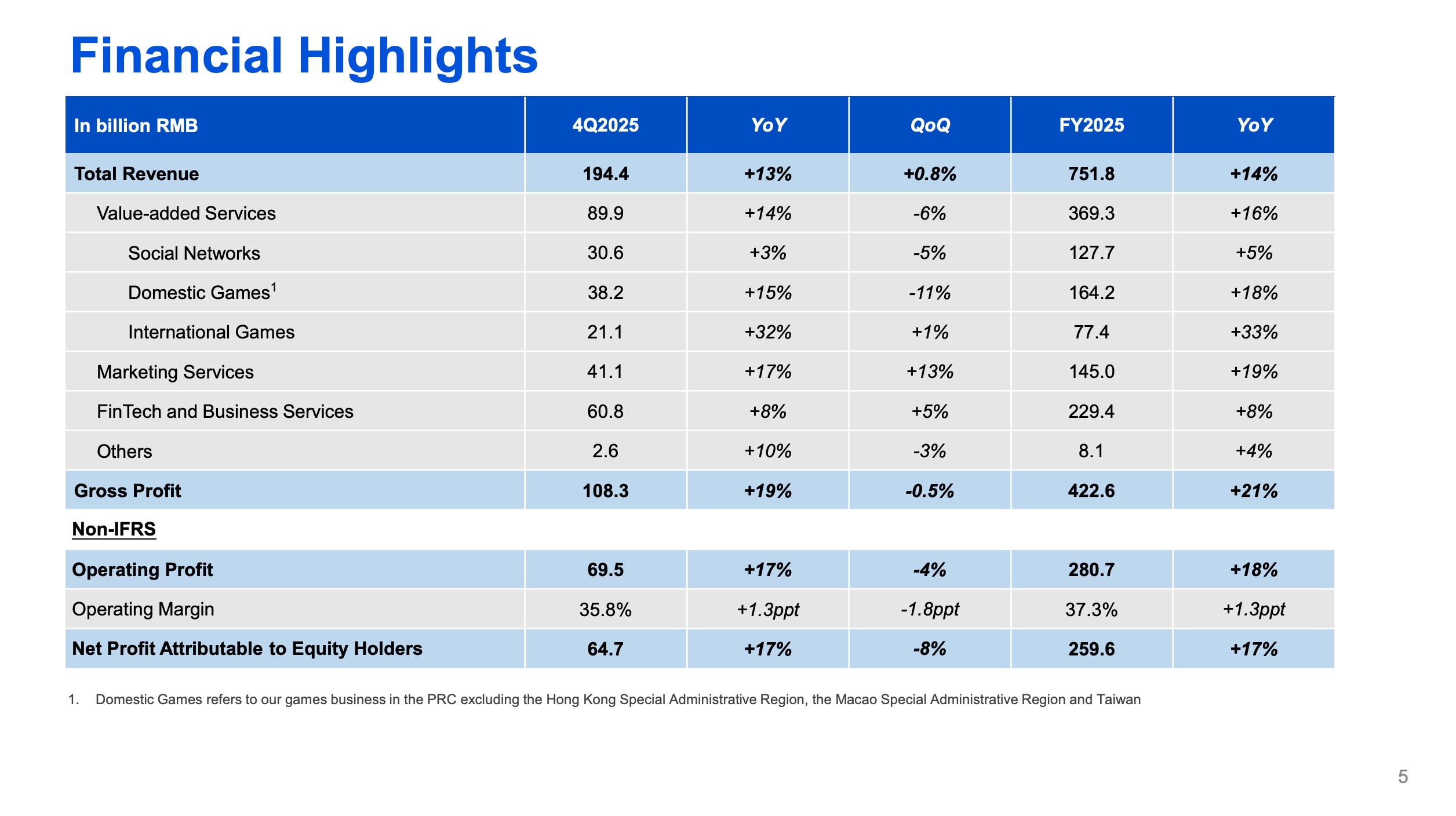

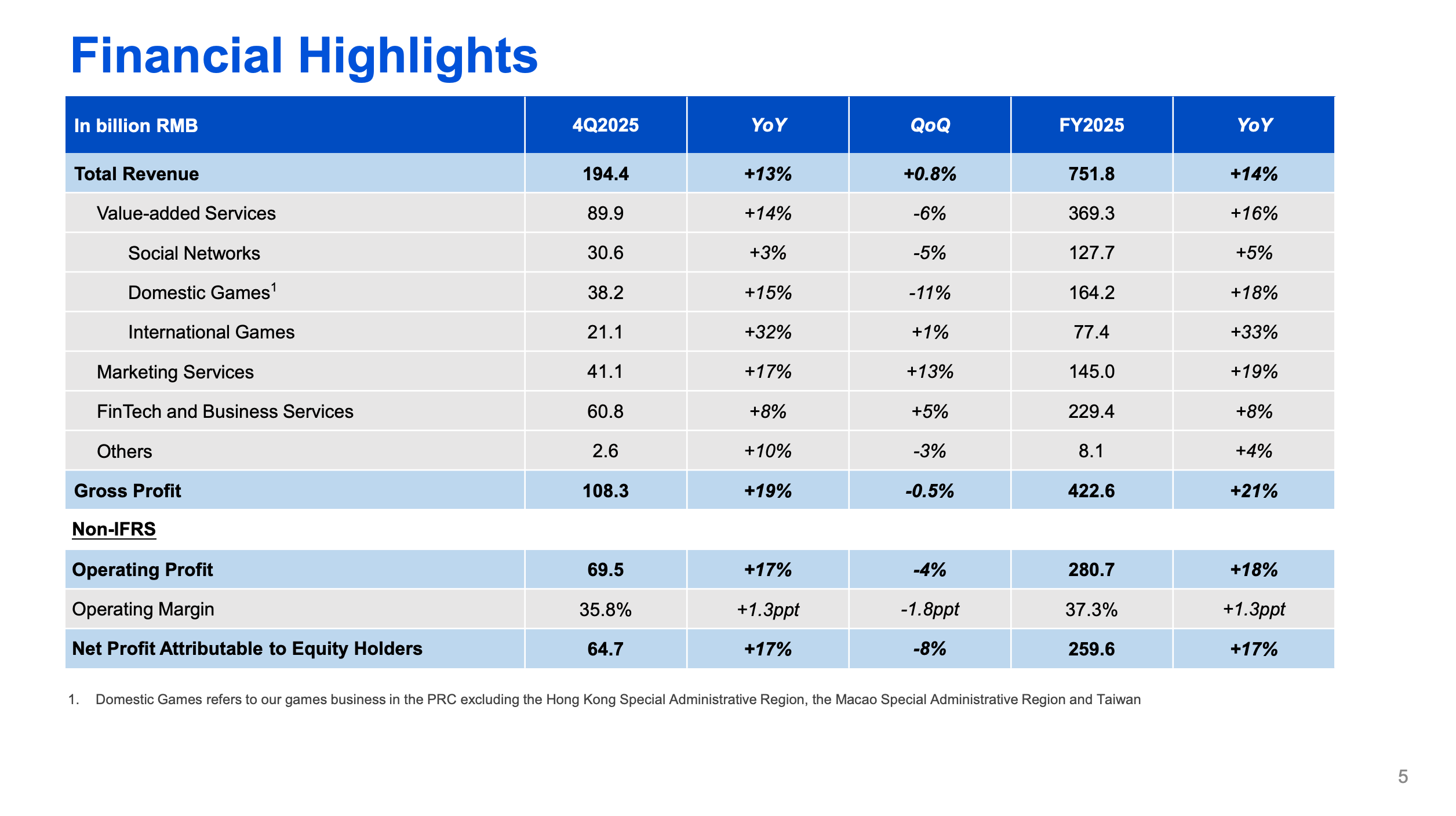

In 2025, Tencent reported RMB751.8 billion of revenue, up 14%.

VAS: RMB369.3 billion, up 16%, about 49% of revenue

Marketing Services: RMB145.0 billion, up 19%, about 19% of revenue

FinTech and Business Services: RMB229.4 billion, up 8%, about 31% of revenue

Others: RMB8.1 billion, about 1% of revenue

VAS includes domestic games, international games, and social networks. In 2025, domestic games revenue was RMB164.2 billion, international games revenue was RMB77.4 billion, and social networks revenue was RMB127.7 billion.

The part I care about most is not only the segment split. It is the platform position. Weixin (WeChat) had 1.418 billion combined monthly active users at the end of 2025.

For many users, WeChat is not just an app. It is where they message, pay, use services, interact with merchants, use mini programs, watch content, and move through large parts of daily digital life.

That makes Tencent different from a company that only competes by cutting price or spending more on customer acquisition. Tencent still has competition, and I do not want to pretend it does not. But many businesses also need to work with the ecosystem. Merchants, advertisers, developers, payment users, game studios, cloud customers, and service providers all touch parts of Tencent.

This is why I see Tencent closer to a digital infrastructure business with several profit pools attached to it.

Growth Drivers

Tencent has several very profitable segments, and many of them still have growth tailwinds. Games are still the main profit engine. Advertising is getting better. Payments and fintech continue to grow. Cloud looks more disciplined than before. Mini Programs make the WeChat ecosystem stronger.

Marketing Services can grow if user engagement stays strong in Video Accounts, Weixin Search, Mini Programs, Mini Shops, and better ad targeting. FinTech and Business Services can grow through commercial payments, wealth management services, consumer loan services, cloud services, AI-related cloud demand, and e-commerce technology service fees.

Games can grow through both domestic and international games, but gaming always has content-cycle and regulatory risk.

The other growth driver is Tencent’s ecosystem and investment muscle. Tencent has invested in public and private companies for many years, and in some cases those companies also connect back to Tencent’s ecosystem, but I would separate that value from Tencent’s operating growth.

Kaspi.kz is one example. Kaspi ($KSPI) announced in April 2026 that Tencent invested alongside Kaspi’s co-founder and other long-term investors in the purchase of 6.0 million ADSs from Baring Fintech Venture Funds. Kaspi called Tencent one of its largest shareholders.

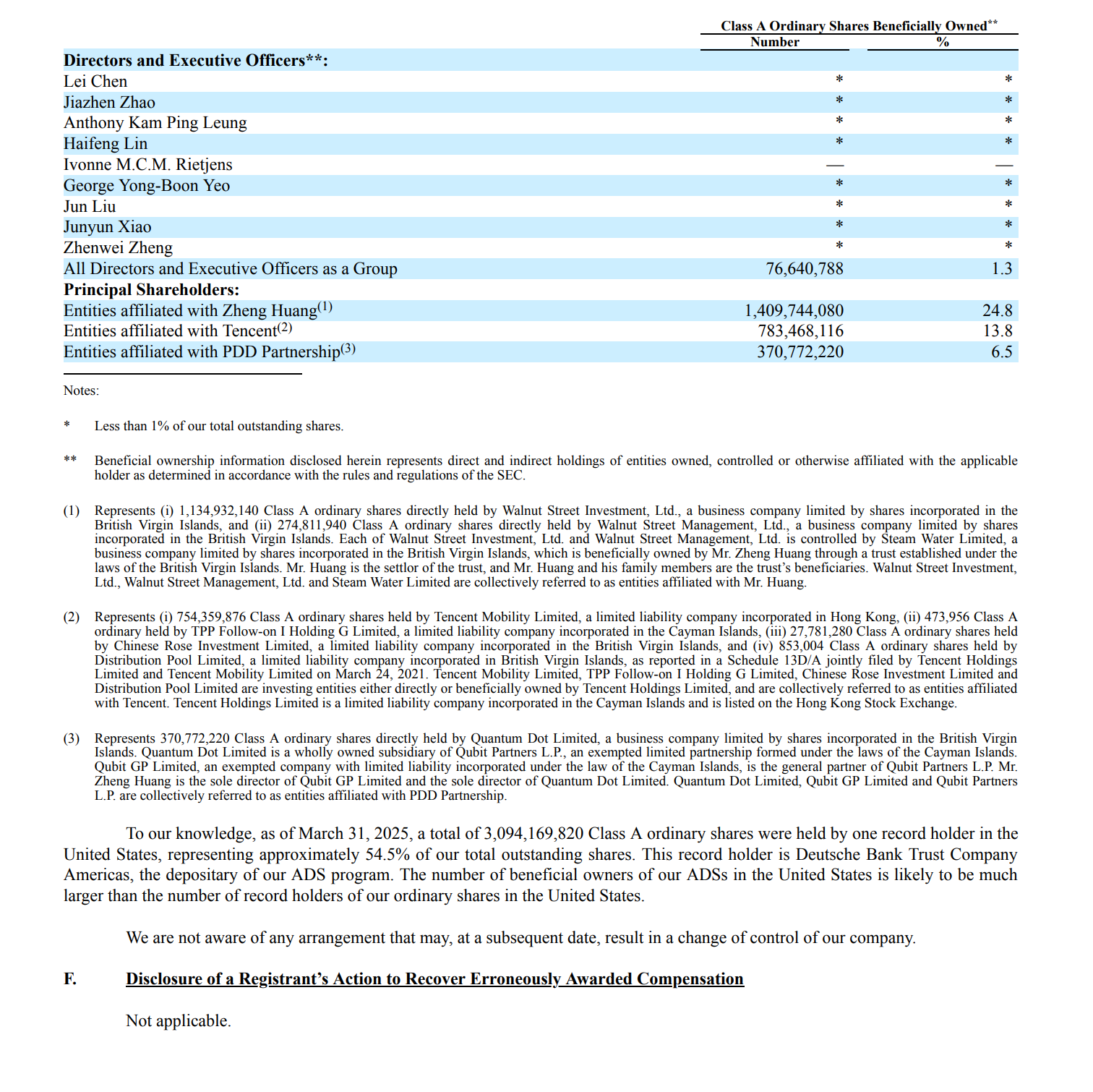

PDD is another useful example. Tencent is still a major shareholder in PDD, owning 13.8% of PDD’s Class A ordinary shares through entities affiliated with Tencent. The two companies have also had a strategic cooperation relationship since 2018, including access points on Weixin Pay, payment solutions, cloud services, user engagement, Weixin payment services, and technical support. PDD also said that in 2023 it signed new agreements with Tencent for continued access points on the Weixin platform.

Tencent is not only an operating company. It also has an ecosystem and portfolio layer around other digital businesses.

Margin / Free Cash Flow Drivers

The financials are one reason I keep following Tencent quarter by quarter. China has been a difficult market since 2020, but Tencent’s profits and cash flow have held up much better than Alibaba’s and many other large Chinese names.

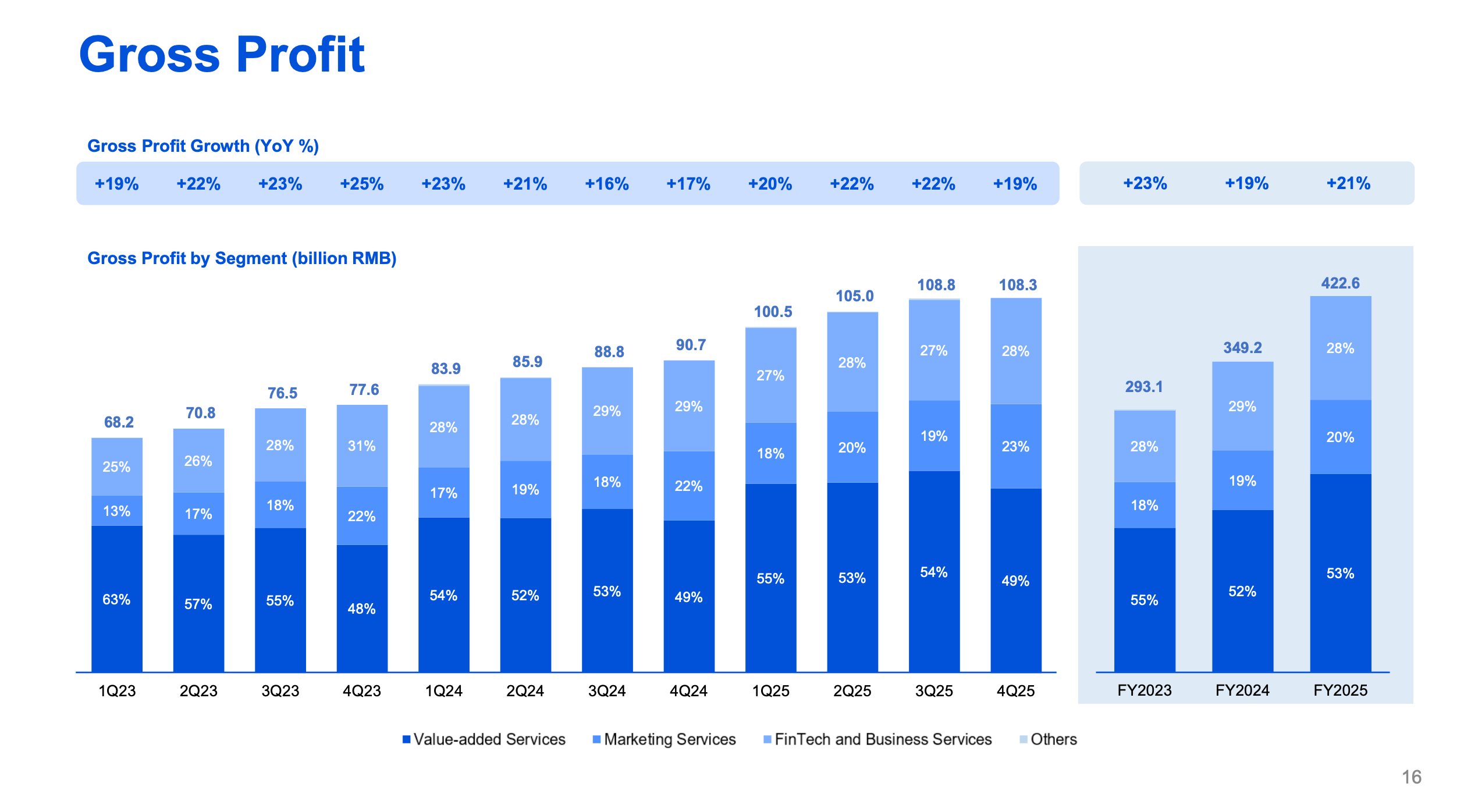

Between 2021 and 2025, Tencent’s revenue grew from RMB560.1 billion to RMB751.8 billion. But the more interesting part is what happened below the revenue line. Gross profit increased from RMB245.9 billion to RMB422.6 billion.

IFRS operating profit increased from RMB124.7 billion to RMB241.6 billion. Non-IFRS profit attributable to shareholders increased from RMB123.8 billion to RMB259.6 billion.

So Tencent did not just grow. It became more profitable during a very tough period. That matters because the environment was difficult for everyone, including Tencent. Broader economic activity slowed down, and many Chinese internet companies struggled to protect margins and cash flow.

The difference becomes clearer when you compare Tencent with Alibaba.

Alibaba Has Doubled — Why I’m Cautious

·Alibaba Group Holding Limited (BABA) is up more than 100% since I first wrote that it was undervalued.

As I wrote before, Alibaba’s revenue growth became more expensive. Margins were pressured, and free cash flow declined. Tencent was different. Revenue grew, but profits grew faster. Margins improved, and free cash flow stayed strong.

Gross margin improved from around 44% in 2021 to 56% in 2025. IFRS operating margin improved from around 22% to 32%.

That matters because revenue growth alone can be misleading. What I want to see is whether more of each renminbi of revenue is turning into profit. In Tencent’s case, that has clearly happened.

For FY2025, Tencent reported RMB751.8 billion of revenue and RMB422.6 billion of gross profit. More importantly, the business generated RMB182.6 billion of free cash flow, up 18% for the year. Tencent also ended the year with RMB107.1 billion of net cash.

Capital Allocation

Capital allocation is one of the main reasons Tencent is interesting. I do not want to overdo the Berkshire ($BRK.B) comparison, but there is one simple similarity: Tencent has used operating cash flow to own stakes in many other companies over time.

At the end of 2025, Tencent reported RMB672.7 billion of listed investee company shareholdings at fair value and RMB363.1 billion of unlisted investee company shareholdings at carrying value.

Tencent also repurchased 153.4 million shares for about HKD80.0 billion in FY2025 while ending the year with RMB107.1 billion of net cash.

That combination matters to me because the company can reinvest in games, cloud, AI, payments, and WeChat, while also buying back shares and keeping financial strength.

The shareholder structure is also worth noting. As of 31 December 2025, MIH Internet Holdings B.V., controlled by Naspers through Prosus, owned 22.8% of Tencent. Ma Huateng, Tencent’s co-founder, had an 8.82% interest through Advance Data Services.

Market Concern

The market has real reasons to be cautious. Tencent is Chinese, complicated, and exposed to regulation, gaming approvals, geopolitics, currency, consumer weakness, AI spending, and the wider discount investors apply to Chinese equities.

There is also one honest limitation. I do not live in China. I can read the annual reports and filings, but that is not the same as using the ecosystem every day. Tencent is tied to how people in China communicate, pay, shop, play games, consume media, and use services. It is also tied to local regulation. Because of that, I need a bigger margin of safety than I would need for a business I understand directly as a customer.

Bear Case

The bear case is not that Tencent is a bad business. The bear case is that Tencent can be a very good business and still not be a good investment for a foreign investor if the discount is not large enough.

Regulation can change. Gaming approvals can affect the profit engine. Consumer behaviour can weaken. AI and cloud spending can pressure free cash flow if returns are not good enough. The investment portfolio can be hard to value, especially the unlisted part. Minority shareholders may not receive the full value of the portfolio in the simple way a spreadsheet suggests.

There is also the risk that I overestimate the ecosystem because I am looking from outside China. WeChat may be critical to daily life, but I still need to understand what can weaken that position, what can become more competitive, and what the government may allow Tencent to earn over time.

This is why the short thesis matters more than the long thesis at the start. It is easy to say Tencent is high quality. The harder question is why I might be wrong.

Valuation Question

As of today, Tencent trades at HKD471.40, with a market value of around HKD4.3 trillion and a P/E of about 17x.

Tencent trades at around 20–21x FY2025 free cash flow based on the headline market cap. That is not deep value by itself.

The valuation becomes more interesting when I adjust for the balance sheet and investment portfolio. Tencent had RMB107.1 billion of net cash and RMB672.7 billion of listed investee stakes at fair value. If I give credit to those two items, the operating business looks closer to a mid-teens multiple of FY2025 free cash flow.

If I also give full credit to the unlisted investments, the multiple looks even lower. But I would be careful with that. Unlisted investments are not cash. I do not want the thesis to depend on treating them as cash.

So the valuation question for me is simple:

After cash, listed investments, the broader portfolio, and China risk, is the price attractive enough for the quality of the business?

What Must Remain True

Tencent is already part of the infrastructure of daily life in China.

Weixin and WeChat are not just apps. People use them to communicate, pay, shop, access services, follow content, play games, interact with merchants, and move through the digital economy. That is what makes Tencent different. It is not just another internet company trying to compete on price.

This is why I am less worried about normal competition. Competition always exists, but Tencent’s position is very hard to replicate. The bigger risks for me are regulation, China risk, and how much profit Tencent is allowed to earn from such an important position over time.

The business already has very profitable segments. Games, advertising, payments, fintech, cloud, and business services all sit inside a very strong ecosystem. The important thing is not whether Tencent suddenly becomes profitable. It already is. The question is whether those economics remain strong and whether free cash flow continues to hold up.

Management is also one of the reasons Tencent is interesting. This is not a weak management team with no history. Tencent has a strong track record, highly capable leadership, meaningful insider ownership, and a long-term way of thinking. Ma Huateng still has a serious economic interest in the business, and that matters to me. It does not guarantee perfect decisions, but it changes how I read capital allocation.

I want management to keep doing what they have mostly done well: allocate capital rationally, protect the strength of the core business, invest where returns make sense, and return capital when the stock price is attractive.

I do not want to own Tencent only because the stock is below its old high. I would only want to own it if the business quality, cash generation, balance sheet, investment portfolio, management quality, and price together compensate for the risks.

What Would Prove Me Wrong

I would be wrong if Weixin started to lose their role as daily digital infrastructure in China.

The real risk would be deeper than normal competition: people using the ecosystem less, merchants becoming less dependent on it, Tencent losing pricing power, or the company losing the ability to monetise its position. As of today, I think that outcome is very unlikely.

I would also be wrong if regulation permanently damaged the economics of the business. The government can change rules, gaming approvals can affect the profit engine, and policy can limit how much profit Tencent is allowed to earn over time.

Competition is still worth watching, but I am less worried about competition alone because Tencent’s position is already very strong. What would worry me more is competition plus regulation plus changing user behaviour weakening the platform over time.

I would also be wrong if margins reversed without a clear future return, if free cash flow weakened structurally, if AI and cloud spending consumed too much cash without good returns, or if the investment portfolio could not be monetised in a way that benefits shareholders.

Tencent can be a great business and still become a poor investment if the price does not leave enough margin of safety.

Not investment advice. Just my own thinking.

The AI question is the real one for me. The market is voting saaspocalypse. Agents replace the super app, terminal value decays. But I think it's at least two stacked things, not one.

The moat isn't uniform. Identity, payments, social graph. Agents will go through those, not around them. Mini Programs, commerce, content discovery. Those are the contestable parts, and Douyin's already eating into them more visibly than any AI agent. Which layer is compounding from here is the actual question.

The other thing I'd push back on is Hunyuan being read as a weakness. It's not first tier, true. But the public moves have been distribution-first. DeepSeek inside Yuanbao. DeepSeek and Hunyuan inside Weixin Search. Same playbook they've always run. Own the surface, plug in whoever has the best model that month. The bet is distribution outlasts model differentiation. Could be wrong. It's a different trade from "Tencent lost the AI race."

Two bear cases, not one. The mispricing depends on which one is right.

Great analysis, specially for the honesty with your own knowledge boundaries. That's rare and crucial for a great investor.