Salesforce Valuation Analysis: 13x Free Cash Flow

A look at current valuation, stock-based compensation trends, and the AI strategy

I’ve been watching Salesforce for years, but it was always priced like the market assumed everything would go right, and I wasn’t willing to play that game. What changed is not just Salesforce, it’s the whole software tape. SaaS valuations have been resetting across the board, and AI made it worse because investors are repricing both “AI SaaS” and “non-AI SaaS” at the same time, mostly out of uncertainty, so prices are moving first and narratives are catching up later. That creates a lot of noise, and it’s easy to confuse a multiple compression cycle with a real business problem

We need to separate signal from noise.

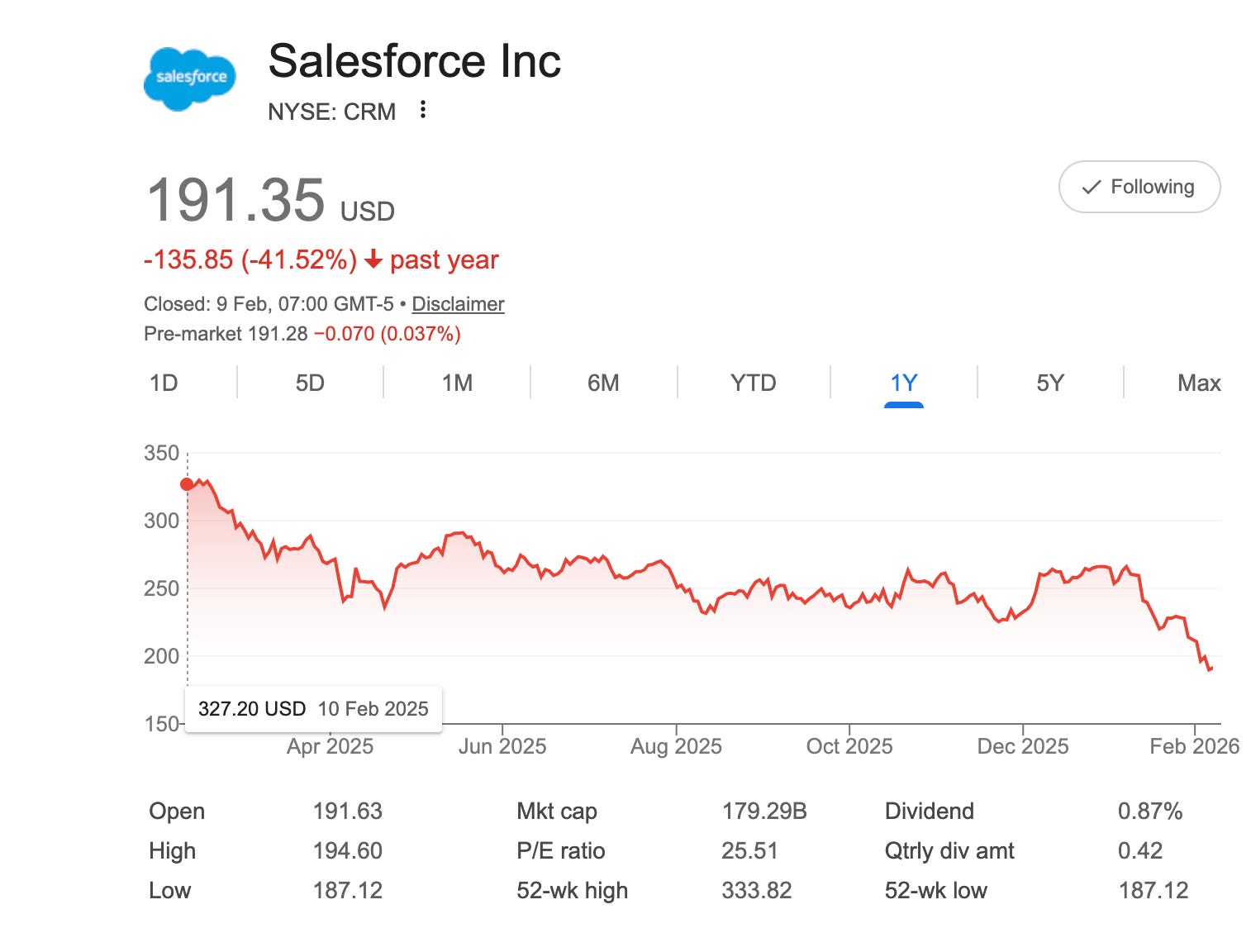

Now Salesforce trades around 13–14x free cash flow. The S&P 500 is closer to 21x. Coca-Cola is around 22x and grows slower. That gap tells you expectations have flipped, the market isn’t paying for the best case anymore. At 14x, Salesforce doesn’t need to prove it can grow at 20% to make sense; it just needs to stay stable, keep customers, and keep converting revenue into cash.

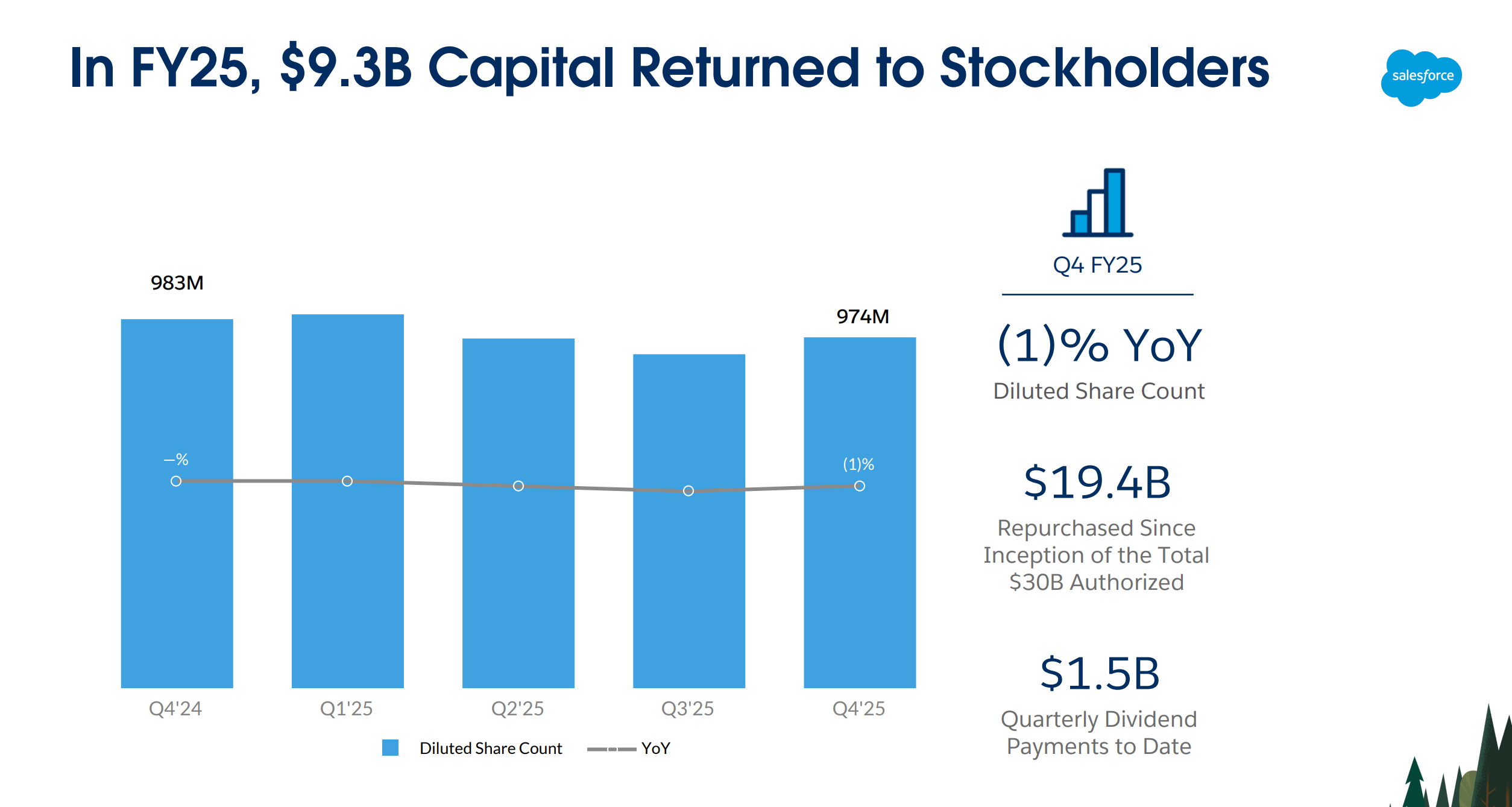

They’re managing costs better

Stock-based comp is now around 8% of revenue, down from over 10%. They also stopped hiring as many people. When costs slow down and revenue stays the same, profits go up.

This is the first time in a while the company seems to care about shareholders.

Customers don’t leave easily

About 90% of the Fortune 500 use Salesforce. It’s not just software. It holds years of customer data, workflows, integrations, and reports. You can’t just turn it off. Replacing it takes years and comes with risk.

So even if growth slows, the customer base stays.

It’s an Ecosystem, Not an App

If Salesforce were just a place to store phone numbers, you could export a file and switch to a competitor in an afternoon. But for the Fortune 500, Salesforce is more like an operating system.

Companies build custom applications on top of Salesforce using proprietary languages like Apex and tools like Flows. These custom apps do not translate to other systems. To leave, you have to rebuild them from scratch.

A typical enterprise has Salesforce connected to their ERP system, their marketing tools, their customer support lines, and their email. Unplugging Salesforce breaks the data flow across the entire company.

Data Gravity

As a dataset grows, it becomes harder to move.

Years of customer interactions, purchase history, and support tickets are stored there. Migrating this data to a new structure is a large project with a high risk of corruption or loss.

Most companies have messy data. Moving requires cleaning it first—a project that can take months on its own.

The “Rip and Replace” Risk

Replacing a core system like Salesforce is often compared to changing the engine of a plane while it is flying.

If the new system fails or has bugs during the switch, sales stop, support tickets get lost, and revenue takes a direct hit.

You have thousands of employees who know exactly where to click to do their jobs. Moving to a new interface causes a large dip in productivity for 6–12 months as users relearn how to work.

What could go wrong

The stock is cheap for a reason.

If teams start working through AI agents, they might not log into Salesforce anymore. The AI just talks to Salesforce in the background. If Salesforce becomes invisible, they lose pricing power.

Salesforce charges per user. If AI makes teams more efficient, companies need fewer people. Fewer people means fewer licenses. The question is whether they can replace that revenue fast enough with usage-based pricing.

Why I’m looking at it now

At $175–$190, Salesforce isn’t priced like it has to keep growing fast.

If it becomes like Oracle with customer data, that’s not exciting, but it can generate cash for years. And at ~13x free cash flow, the market already treats it that way.

That’s the point and that’s why it’s worth watching.

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier