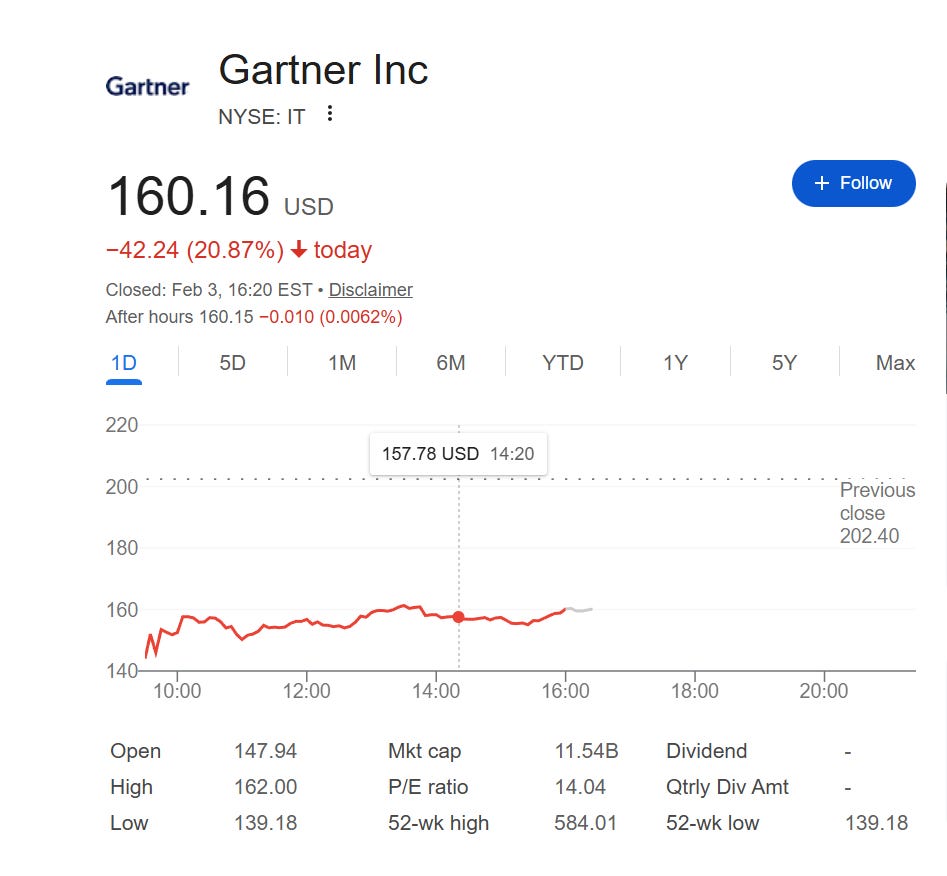

Gartner brought down a lot of SaaS and tech stocks today. The Nasdaq was down about 2% as well.

What surprised me was the lack of real coverage that explained what actually happened. Most posts just repeated the headline: “Gartner missed” or “guidance”.

Adjusted EPS was $3.94. Revenue grew 2% to $1.8 billion. Free cash flow was $271 million in the quarter.

They bought back $500 million of stock in Q4 and $2.0 billion for the full year.

The stock still fell because the market fixated on one metric: contract value growth.

In Q4, global contract value reached $5.2 billion but grew only 1% year over year. Ex-U.S. Federal, growth was 4%. That number alone was enough to change perception. Not because it is a collapse, but because it is far from what investors were used to paying for.

This was not driven by client losses.

Clients are renewing. In Global Business Sales (GBS), client retention was 86% and wallet retention was 99%. The issue was expansion. Companies are keeping Gartner but delaying decisions to add seats, expand usage, or increase scope.

Management described the pattern as budgets are under pressure, approval levels are higher, and buying cycles are longer. When spending decisions move from CIOs to CFOs, expansion slows first. Renewals hold, but growth inside the account gets harder.

Government was a clear headwind.

U.S. Federal clients faced efficiency initiatives and funding changes, and management said this reduced contract value. They also said that at year-end they had only $126 million of U.S. Federal contract value remaining. Ex-federal growth was roughly 330 basis points higher, which helps isolate the impact.

But it was not only government.

In the core Global Technology Sales (GTS) segment, which is roughly $3.9 billion of the total business, contract value was flat year over year. That matters because it shows the behaviour across private enterprise too. This was not a single customer problem. It was broad budget behaviour.

Some investors pointed to AI as the cause. Management pushed back on that.

They said they track whether clients raise AI as a substitute during sales and renewal conversations, and they do not see it as meaningful. They also said AI is the biggest topic clients ask about. Gartner said it produced over 6,000 AI-related documents and had about 200,000 in-depth client conversations on AI in 2025. The message was simple: clients are not replacing Gartner with AI tools. They are using Gartner to make AI decisions.

The seat model is still the pressure point.

Gartner’s model works best when organisations are hiring. Hiring has been flat. When employees leave and roles are not refilled, seats get removed. That hurts expansion even when the relationship is stable.

Management is responding by trying to increase engagement and speed so the value stays clear even when headcount does not grow. They gave an example: they reduced creation time for some high-value research outputs (like Magic Quadrants) by 75%.

Why does that matter?

Because Gartner compounds through renewals. More engagement now can show up as higher contract value later, often 12 to 24 months later when contracts come up for renewal. The company is investing now to affect that later outcome.

Management guided for 2026 revenue of at least $6.455 billion and adjusted EPS of at least $12.30. The market did what it always does: it discounted uncertainty immediately.

Why the market listened, and why other software names moved

Gartner is a read-through on enterprise budgets.

When Gartner says expansion is slower because approvals are tighter and buying cycles are longer, the market applies that logic across other companies that rely on seat growth, upsells, and budget confidence.

That’s why names like $CRM, $NOW, $SAP, and $TTD moved with it. Different products, same behaviour: expansion is the first thing customers delay.

The Nasdaq was down about 2% on the day. In that kind of market, any confirmation of slower demand leads to multiple compression. This was not “bad news.” It was “less certainty.”

Valuation reset

When a stock drops hard, investors assume the business is in trouble. Sometimes that is true. But sometimes the business is fine and the market is repricing the stock because the growth story changed.

The cash flows can still be there. Retention can still be there. Margins can still be there. What changes is the expected pace of expansion, and the multiple investors will pay while they wait.

That is what this felt like.

Gartner did not show stress in the core subscription model. Renewals held, margins held, and buybacks continued. The market reaction was about contract value growth slowing, which reduces confidence in the next 12–24 months.

When confidence drops, the multiple compresses first. The income statement follows later, if the slowdown persists.

Valuation

Disclaimer: This article is for informational purposes only. It is not financial advice. I am not a financial advisor. I may buy or sell these stocks at any time. You must do your own research before investing

By reading this email, you agree to the full disclaimer found here: https://www.thevaluethesis.com/p/disclamier