Booking Holdings (BKNG) Business Model & Moat Analysis

A deep dive into the unit economics, the shift to merchant payments, and why Booking.com is the trust layer of global travel.

Hello fellow investors,

I am about to introduce a new section called Business Analysis, where I will be publishing work under Business of the Week.

Most investors make the mistake of focusing too much on the numbers and not enough on the business behind the numbers.

So I decided to start publishing my business research notes in article format more regularly. This will be a place where I break down businesses that I think are worth knowing, studying, and understanding better.

The goal is to understand how a business works, how it makes money, where the economics come from, and what makes it interesting.

Thank you for being a subscriber and for reading my work. If you find value in these breakdowns, please feel free to forward, share, or like them. If you are on the free tier, you can support this work directly by upgrading to a paid subscription, and to those who are already paid members, thank you for making this deep-dive research possible.

Disclaimer: This article is for informational and educational purposes only. It is not investment advice or a recommendation to buy or sell any security. Just my opinion. Please do your own due diligence before making any financial decisions.

Summary

Booking is mainly an accommodation business, even though it also owns Priceline, Agoda, KAYAK, OpenTable, and Rentalcars.com.

The business is useful because travel booking still has a lot of friction: reviews, payment, cancellation, confirmation, support, and trust.

For travellers, Booking reduces uncertainty. For hotels, it brings demand they may not easily get on their own.

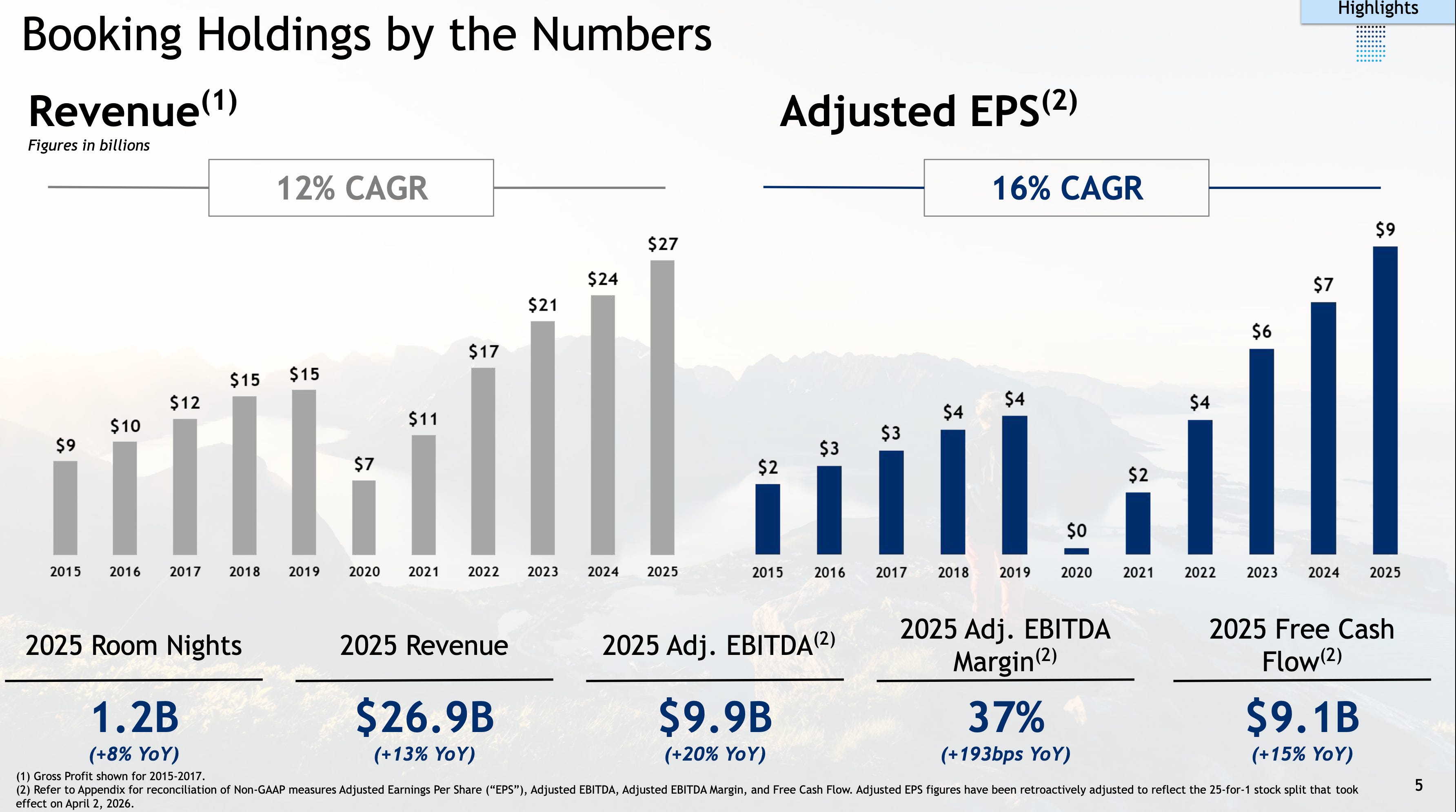

In FY2025, Booking generated $26.9 billion of revenue and about $9.1 billion of free cash flow, with very little physical capex.

The moat is real, but it is not hard lock-in. It comes from supply, demand, reviews, trust, payment confidence, customer support, and app habit.

Marketing is the main economic cost to watch. If Booking is building direct customer habit, marketing can be valuable. If it is only buying the same demand again and again, the business is less powerful than the headline cash flow suggests.

Google and AI may be bigger risks than other OTAs because they sit before the booking decision and could control where travel demand starts.

My view: Booking is a high-quality business, but its quality depends on whether it can keep turning trust into direct customer habit and AI is a risk, especially if Booking does not turn more customers into loyal mobile app users. In the future, people may ask an AI agent to plan and book a trip, and that agent may decide where the demand goes

Booking Holdings

When I book a holiday, especially with family, I am not just choosing a hotel room.

I am thinking about the whole trip.

I want to know where we will stay, how easy it will be to get there, whether the place feels right, whether the reviews are honest, and whether I can trust what I see on the screen.

Because a holiday is not just another purchase. You spend real money, you plan around it, and often you look forward to it for weeks or months.

And when something goes wrong, it does not feel like a small inconvenience. It can affect the whole experience.

I felt this myself recently during a trip abroad.

Booking.com could not really help with one of the places because it was not available on their end, so I had to deal directly with the hotel myself.

And once you do that, you realise how much friction there can be in travel. The booking, the communication, the reservation, the payment, checking the details, trying to explain something to hotel staff who may not speak the same language, even simple things can become frustrating when you are travelling.

All of these small problems add friction, especially when you are in another country and just want the trip to go smoothly.

That is why Booking is interesting to study. From the outside, it looks like a simple website for hotels and flights. But underneath, it is solving a very emotional and practical problem: helping people make travel decisions with less uncertainty.

Booking Holdings is a global online travel marketplace. Its main business is accommodation, mostly through Booking.com, but it also owns Priceline, Agoda, KAYAK, OpenTable, and Rentalcars.com. Travellers use it to find, compare, review, reserve, and pay for hotels and other travel products. Hotels and accommodation partners use it because Booking brings them demand they may not reach directly. Booking makes money mainly from merchant and agency travel reservation revenue, plus advertising and other revenue.

Travel booking has friction everywhere. When you book a trip, you are trying to balance many things at the same time: price, location, flexibility, reviews, payment, and trust.

A cheaper room does not mean much if you are not sure about the place. Good cancellation terms do not help much if the confirmation itself feels uncertain. And when you are travelling to a country you do not know, with a hotel brand you do not know, even small things like currency, payment, and cancellation can feel risky.

This is where Booking becomes useful. It reduces some of that uncertainty and makes the decision feel easier.

Booking takes all of that mess and makes it easier. It does not remove every travel risk, but it reduces enough of the risk that customers come back.

The direct hotel option is not always easy either. If I do not know the hotel, I may not feel comfortable putting my card details into its website. I may not be sure if the payment will go through safely. I may not fully understand the cancellation rules. And if something goes wrong, I may not know how easy it will be to get help.

This is where Booking becomes useful. It puts the search, reviews, price, payment, confirmation, and support in one place, and makes the whole process feel less risky.

For hotels, Booking solves the other side of the problem. A hotel may have rooms, but not enough direct demand. Booking gives it global visibility. That creates the marketplace loop: travellers come because there is supply, and hotels stay because there is demand.

The customer is not only searching for the cheapest room; they are trying to avoid a bad trip. A failed hotel booking has a high emotional cost because if the room is not there, the property is bad, or the hotel is oversold, the customer cannot just “return the product” and move on while the trip is already happening.

Booking.com

The most important product is Booking.com. This is the core accommodation engine and the place where the strongest customer habit sits.

Agoda matters in Asia, while Priceline matters more for U.S. and discount travel. KAYAK provides metasearch, Rentalcars.com supports connected trips, and OpenTable adds restaurant exposure, but none of those businesses sits at the centre of this thesis.

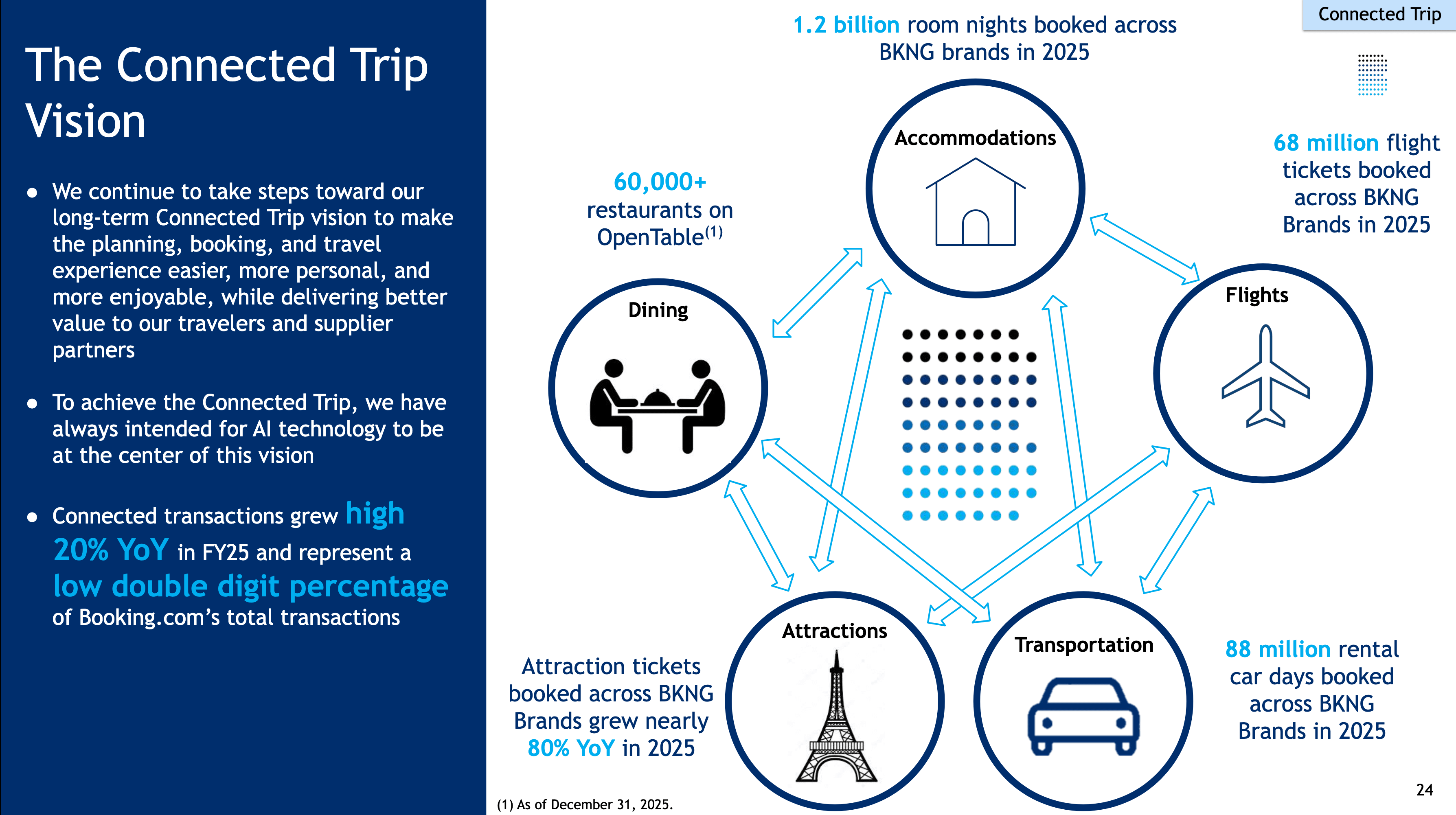

The business should not be analysed as if every product matters equally. Accommodation matters most. Flights, rental cars, restaurants, payments, and connected trip matter if they make Booking more useful and help customers stay inside the ecosystem. They are not automatically good just because they make the app broader.

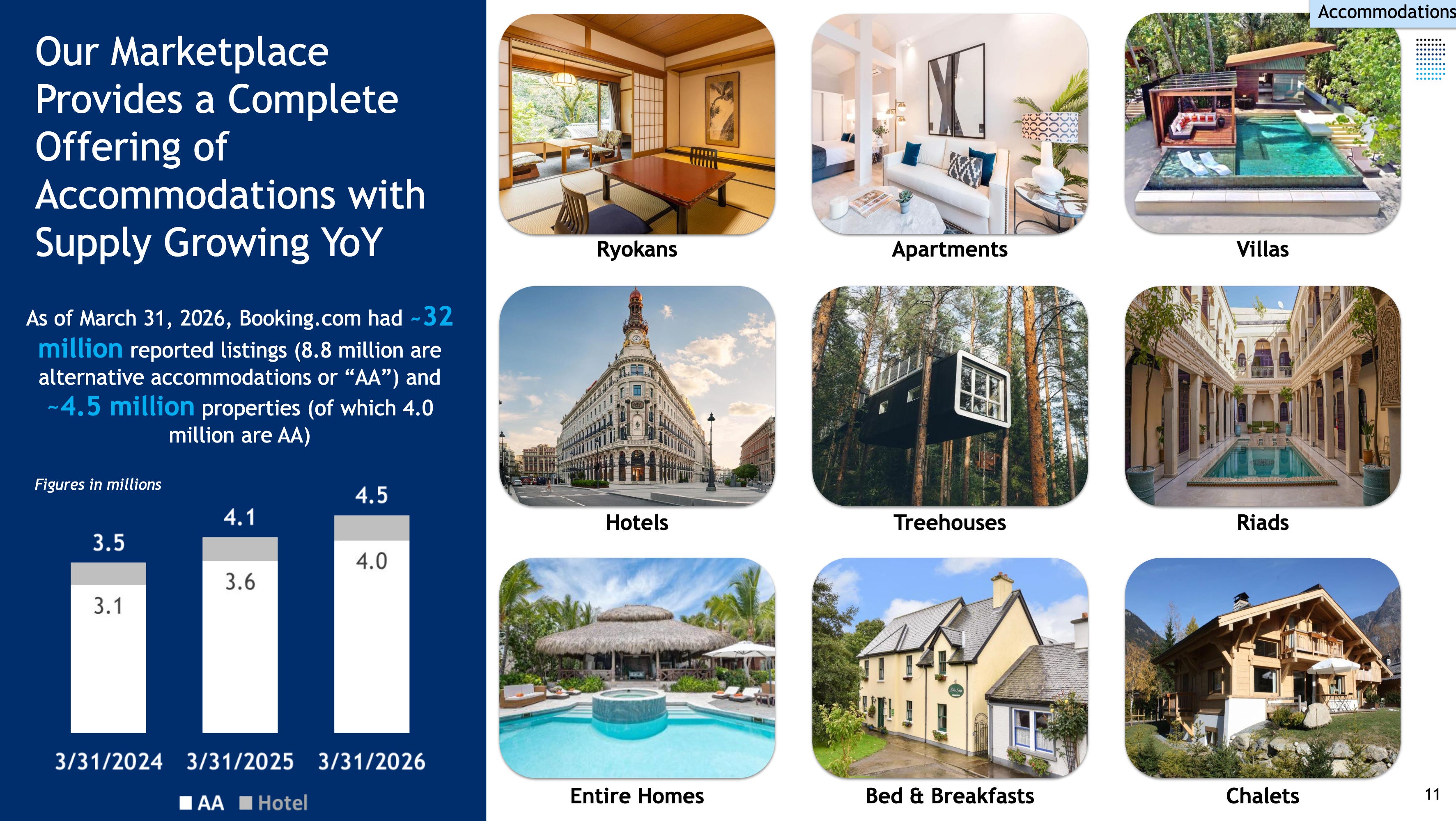

Booking.com had about 4.5 million total properties at March 31, 2026. About 4.0 million were alternative accommodation properties and about 500,000 were hotels, motels, and resorts. Alternative accommodations were about 38% of Booking.com’s Q1 FY2026 room nights.

The Economics

Booking makes money mainly in two ways. In the merchant model, Booking is more involved in the transaction: it can collect payment from the traveller and then pay the supplier, giving it more control over checkout and customer experience while also taking on payment costs, fraud risk, chargebacks, and operational complexity.

In the agency model, Booking earns a commission or fee from the supplier after facilitating the reservation. In FY2025, Booking generated $26.9 billion: merchant was the largest part at $17.8 billion, or about 66% of the total; agency was $8.0 billion, or about 30%; and advertising and other was much smaller at $1.2 billion, or about 4%.

FY2025 gross travel bookings were $186.1 billion, with $130.1 billion coming through the merchant model and $56.1 billion coming through the agency model.

The simple revenue-to-gross-bookings ratio was about 14.5% in FY2025. I would not call that a clean take rate because revenue recognition and mix matter, but it is still useful. It shows how much economics Booking roughly captures from the travel volume moving through the platform.

The important unit-economic question is not only how many bookings pass through the platform, but how much of that demand Booking owns after paying to acquire it and service the transaction. Booking reports room nights, gross bookings, revenue, marketing expense, direct mix and app mix, but it does not disclose customer acquisition cost, customer lifetime value, or profitability for a direct booking compared with a paid booking.

The best observable test is therefore whether more booking volume produces more revenue and cash without marketing taking a larger share of the economics, while direct and app usage holds or improves. FY2025 gives a strong consolidated reading because gross bookings grew 12%, revenue grew 13%, adjusted EBITDA grew 20%, and free cash flow grew 15%, but those group figures do not yet prove that each additional customer or each new U.S. booking has the same quality of profit.

Booking is far more international in its reported economics than the brand list alone suggests. In FY2025, the company reported $24.3 billion of revenue from businesses outside the U.S., about 90% of its $26.9 billion total, while its U.S. businesses generated $2.6 billion, about 10%. Within the international figure, $21.7 billion was attributed to an entity domiciled in the Netherlands, where Booking.com is headquartered.

This breakdown measures the operating business that earns the revenue, not the traveller’s nationality or the hotel location. Booking gives the example that a U.S. customer booking a New York hotel through Booking.com is counted in its business outside the U.S. The numbers therefore show that Booking.com’s international operating base is the centre of group economics, while they do not prove how strong the Booking.com habit is with American travellers.

In FY2025, Booking booked 1.235 billion room nights, up 8%. Gross bookings reached $186.1 billion, up 12%, while revenue grew 13% to $26.9 billion. The more important point is that adjusted EBITDA grew faster than revenue, up 20% to $9.9 billion, and free cash flow grew 15% to $9.1 billion.

In Q1 FY2026, Room nights were 338 million, up 6%. Gross bookings were $53.8 billion, up 15%, or about 8% in constant currency. Revenue grew 16% to $5.5 billion, or about 10% in constant currency, and adjusted EBITDA grew 19% to $1.3 billion. Free cash flow was $3.1 billion, down 2%, but I would not over-read one quarter because Q1 cash flow has seasonality and working-capital timing.

Profit and free cash flow have grown faster than revenue in recent years, which suggests operating leverage, although travel was still recovering from the pandemic base in earlier years and the recent history should not be projected forward as a normal growth rate.

Booking can grow in a few ways. The simple version is more room nights and more gross bookings per room night. The better version is more direct and app bookings, because that means the customer relationship is getting stronger. Alternative accommodation supply can expand the market, merchant payments can give Booking more control over checkout, and connected trip products like flights and rental cars can make the app more useful.

The U.S. could be another growth area, although Booking’s position there is less obvious than its international strength. AI-assisted travel planning could also help if Booking uses it to make the product more personal and easier to use. The risk is that AI helps someone else own the customer relationship instead.

Booking is asset-light, but marketing means it is not cost-light. FY2025 marketing expense was $8.2 billion, about 30% of revenue, which is the key economic cost to understand in this business.

If Booking spends marketing money to bring in new customers who later become direct/app users, that can be good investment. If Booking has to spend more every year just to keep the same demand, marketing starts to look like maintenance capex.

I do not want to look only at reported capex. Booking’s physical capex is tiny, but the real economic reinvestment may be hidden in marketing, product development, AI, payments, and customer service.

Booking manages five operating segments but aggregates them into one reportable segment, so it does not give investors a margin for Booking.com, Priceline, Agoda, or a U.S. versus international business. At group level, FY2025 operating income was $8.8 billion, about a 33% operating margin, while adjusted EBITDA margin improved to 36.9% from 35.0% in 2024. That is excellent, but it does not tell me whether a stronger U.S. push or a wider mix of flights and alternative accommodation would carry the same profitability.

The margin pressure is visible in the model itself. Booking said the shift towards merchant transactions adds payment processing, chargeback, fraud and other costs, and can reduce operating margin even while incremental payment revenue improves earnings. It also said non-accommodation services can have lower margins as they become a larger part of the business. Revenue growth is therefore not enough on its own; the quality of this business depends on what Booking is selling, where the economics sit, and whether the expanding mix keeps the same quality of profit.

Cash flow is the best part of the business because in FY2025 Booking produced $9.4 billion of operating cash flow while spending only about $0.3 billion on capital expenditure, leaving about $9.1 billion of free cash flow, or roughly 34% of revenue.

Booking produced about $9.1 billion of free cash flow in FY2025 with only about $0.3 billion of capex.

The return profile is very strong if direct and app mix keeps improving, because marketing is then building a customer relationship rather than repeatedly buying the same demand. If demand has to be bought again and again, the business is still good, but less powerful than the headline free cash flow suggests.

Trust Must Become Direct Habit

Booking’s moat is strong, but it is not the same type of moat as enterprise software.

There is no hard lock-in. A customer can use another website tomorrow. A hotel can also try to get direct bookings. But Booking has built something valuable through a combination of supply, demand, trust, and habit.

It has a large global supply base, millions of travellers searching and booking, years of reviews, booking history, payment trust, customer support, and service recovery.

The mobile app also helps because over time Booking becomes less of a search result and more of a habit. When people travel, many naturally open the app first.

The supplier side is important too. Many hotels still need Booking because it brings them demand they may not easily get on their own.

Then there is the data and ranking layer. Booking is not just showing hotels randomly. It is trying to match customers with the right property based on price, location, reviews, cancellation terms, availability, and past behaviour.

So the moat is not one single thing. It is the combination of all these small advantages working together.

Customers can open another travel app in seconds, so Booking does not have the hard lock-in of core enterprise software. What it does have is the customer’s memory of where a booking felt safe, and in travel that confidence has value.

I would describe this as a strong trust-and-demand moat, but not an unbreakable lock-in moat. Booking’s direct room nights were a mid-fifties percentage of total room nights over the trailing twelve months ended March 31, 2026, while the app mix was in the high-fifties percentage and most app room nights were direct. Those numbers suggest Booking is not only buying traffic, because a real customer habit is already there.

But management has also said SEO traffic has declined and may keep declining in the short to medium term. Google has always been one of the biggest power centers in online travel, and AI can make this even more complicated. If customers ask an AI agent to plan and book a trip, Booking may not be the first interface anymore.

Booking does not automatically lose if AI changes the interface, but it has to remain useful inside that world rather than merely visible in old search results. It needs to be more agentic, more personalized, and still trusted at the transaction layer, because the risk is not that travel disappears but that someone else owns the customer journey.

Booking competes with Expedia, Airbnb, Google, hotel chains, local OTAs, metasearch, credit-card travel portals, and eventually AI travel agents.

Expedia is still large and strong in parts of the market. In Q1 FY2026, Expedia had $35.5 billion of gross bookings, $3.4 billion of revenue, 113.9 million booked room nights, and $542 million of adjusted EBITDA. Its B2B business is growing quickly, which matters because Expedia can pressure travel supply and distribution even if it does not beat Booking everywhere.

Expedia management also called out the strength of B2B growth. Expedia does not need to beat Booking in consumer hotel search to still become a stronger distribution partner behind other travel platforms.

Airbnb owns a different but powerful customer habit. In Q1 FY2026, Airbnb had 156.2 million nights and seats booked, $29.2 billion of gross booking value, $2.7 billion of revenue, and $519 million of adjusted EBITDA. Airbnb is strongest where customers want homes, space, local stays, and group travel. Management is also pushing the company beyond stays into services, experiences, and hotels.

Google and AI may be a bigger risk than other OTAs, because they sit before the booking decision.

Before someone chooses Booking, Expedia, Airbnb, or a hotel website, they often start with search. If Google or AI tools control that discovery layer, they can influence where the customer goes first.

Hotels and chains are also competitors. They can push loyalty, member discounts, and direct booking. But for independent hotels and international trips, Booking still solves a real trust and demand problem.

If Booking disappeared, customers would use Expedia, Airbnb, Google Travel, hotel websites, credit-card portals, local travel sites, or travel agents. Technically, switching is easy because a customer can open another app in seconds. Emotionally, the decision is harder because they still need to trust the payment, the hotel, and the confirmation that the booking will really be there, which is where Booking continues to have value.

Cash Returns Need Discipline

Booking returns a lot of cash: in FY2025 it produced about $9.1 billion of free cash flow, repurchased $6.4 billion of stock, and paid $1.2 billion in dividends. In Q1 FY2026, it repurchased another $3.6 billion of stock and still had $18.2 billion remaining under the repurchase authorization at March 31, 2026.

The balance sheet gives management room to do this. At the end of Q1 FY2026, Booking had $16.5 billion of cash, cash equivalents, and investments, compared with $18.6 billion of senior notes principal outstanding, leaving rough net debt of about $2.1 billion against a business producing very large cash flow.

Buybacks make sense for a business like this because the company produces more cash than it needs for physical reinvestment, but they create value only if the stock is bought below intrinsic value and management is not starving the business of investment in product, AI, payments, direct traffic, and supply quality. The real test is per-share free cash flow over time.

The balance sheet does not look fragile relative to the cash generation of the business; the bigger risk is whether Booking has to spend more to defend demand, not the debt itself.

Distribution And Trust Can Weaken The Business

The reported revenue base also show how important international operations are for the company. But its position with American travellers is less clear. The U.S. revenue number does not really tell us how strong the customer habit is there, because it is not measured by where the traveller is located. Priceline gives the group a U.S. presence, but Expedia and Airbnb may already have stronger customer habits in that market. If Booking has to spend heavily to build that habit in the U.S., that growth may not come with the same margin profile as its more established international business.

The bigger pressure starts with distribution. Direct room nights and app usage suggest Booking already has a real customer habit, but SEO traffic is under pressure, marketing is still a large cost, and AI could change how people start planning travel. If customers begin asking AI agents to plan and book their trips, Booking may not always be the first place they go. Booking can still remain important if it becomes more personalised, more useful in the app, and still necessary for supply, pricing, payments, and execution. But if someone else owns the customer’s first step, Booking may still do part of the work while losing some control of the relationship.

Product mix is another thing to watch. Merchant transactions can improve the booking experience because Booking has more control over payment and checkout, but they also bring extra costs: payment processing, chargebacks, fraud risk, and more operational complexity. Alternative accommodation helps Booking compete with Airbnb, and flights or connected-trip products may make the app more useful. But more volume is not automatically better volume if those areas have lower margins or weaker economics than the core accommodation business.

The business weakens when Booking has to work harder to keep the same customer. If fewer people go to Booking directly, the habit is not as strong. If marketing becomes more expensive, Booking may be spending more just to stay in front of the customer. If people stop opening the app first, then Google, AI agents, hotel websites, or other platforms have more power over where the customer goes.

And because trust is such a big part of the product, one serious issue around payment, fraud, data, or customer service can damage the relationship quickly. People use Booking because it makes travel feel easier and safer. If that feeling starts to weaken, the moat weakens with it.

The main risk is not that people stop travelling. People will travel. The bigger risk is that Booking becomes less important in the customer’s mind. If customers start their journey somewhere else, Google, AI agents, hotel websites, Airbnb, Expedia, or another platform, Booking may still handle some of the transaction, but it may not own the customer relationship in the same way.

My Business View

Booking is a high-quality travel marketplace because it solves a real problem in travel.

Travel booking still has friction everywhere: reviews, payment, cancellation, confirmation, support, and trust.

This is why I personally trust Booking. In many cases, I prefer to go through Booking rather than deal directly with a hotel I do not know. The direct hotel option can sometimes be cheaper, but it can also bring more friction around payment, communication, cancellation, and support. Still, Booking also needs to stay competitive on price, because customers will compare.

The business has low switching costs, heavy marketing spend, Google and search exposure, AI risk, regulation, and competition from Airbnb, Expedia, hotels, and local players.

The marketing side is one of the parts I do not fully like. The question is whether Booking’s marketing brings in customers once and turns them into loyal direct or mobile app users, or whether the company has to keep paying again and again for the same demand.

AI is also a risk, especially if Booking does not turn more customers into loyal mobile app users. In the future, people may ask an AI agent to plan and book a trip, and that agent may decide where the demand goes. Booking may still be involved in the transaction, but someone else could own the customer’s first step.

The core still looks strong because Booking has scale, cash flow, direct and app habit, global supply, and a customer use case that is easy to understand. I do not think of it simply as an online travel agent. I think of it as a trust layer for global accommodation.