Alibaba Has Doubled — Why I’m Cautious

Deep Dive #2

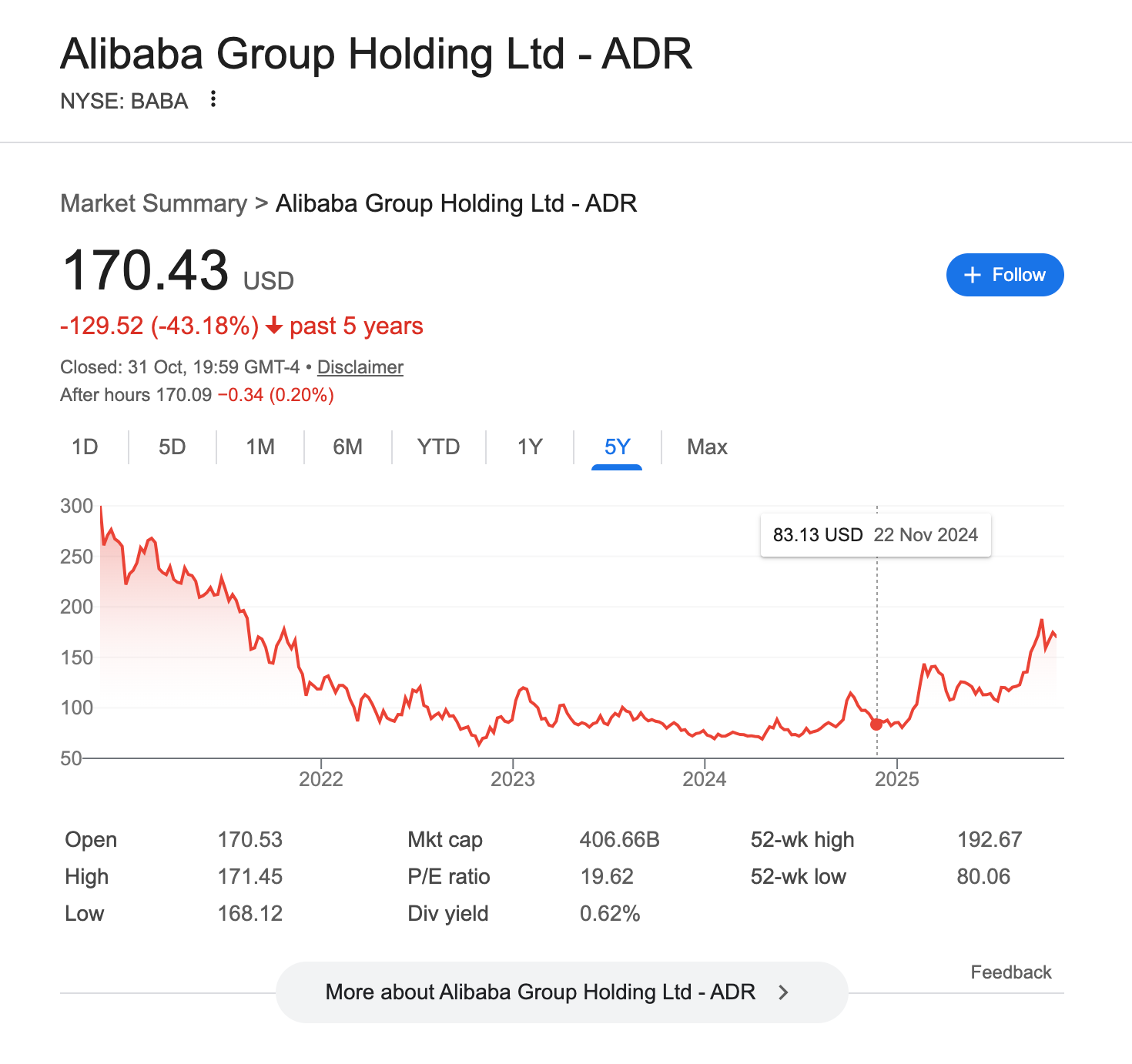

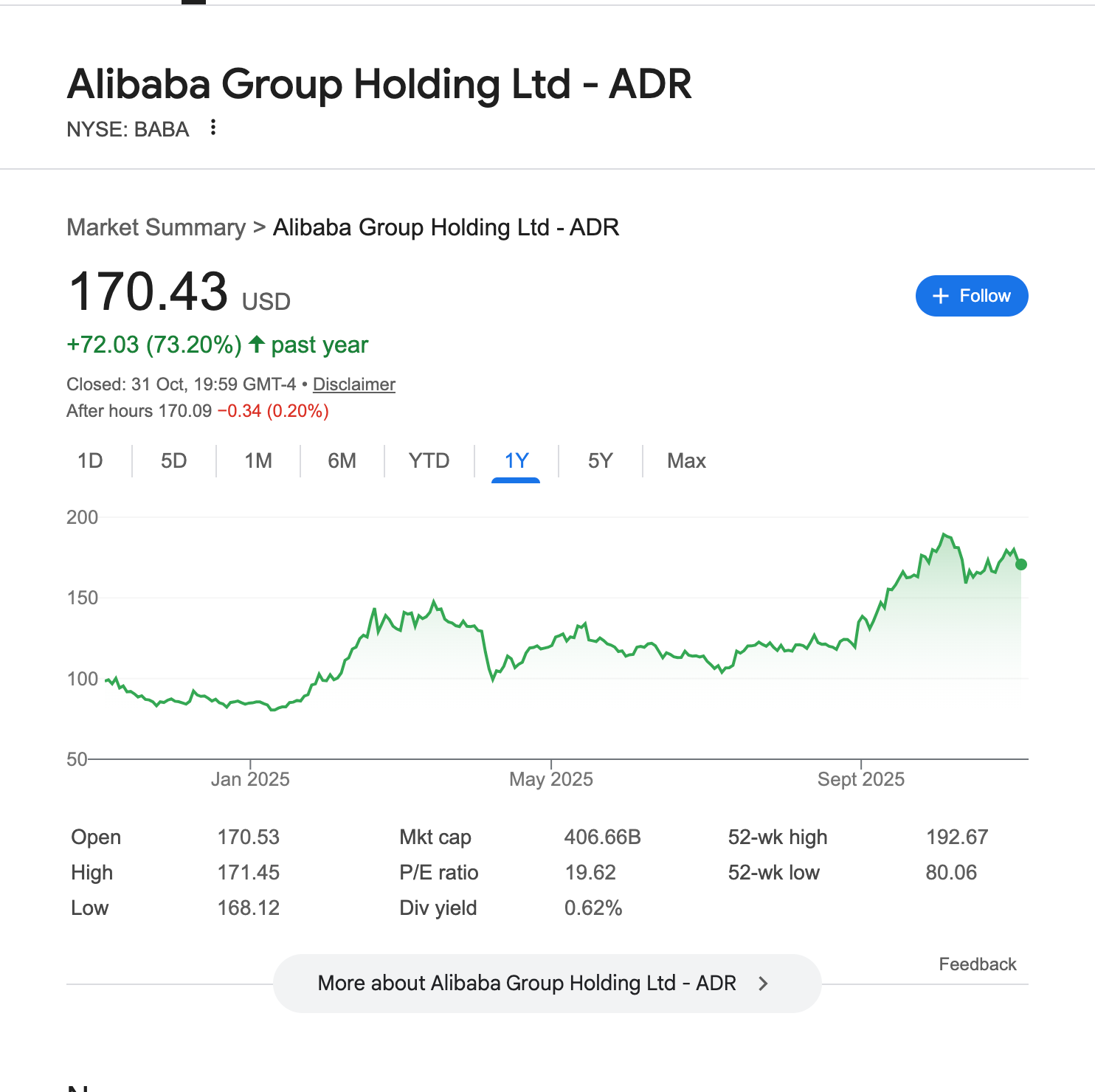

Alibaba Group Holding Limited (BABA) is up more than 100% since I first wrote that it was undervalued.

First, sentiment among investors has improved, and it has changed from “uninvestable” to “investable.”

However, I see some risks and wanted to share them at the current valuation. The price we pay always determines the return, and the risk we take.

Dependence on Taobao and Tmall

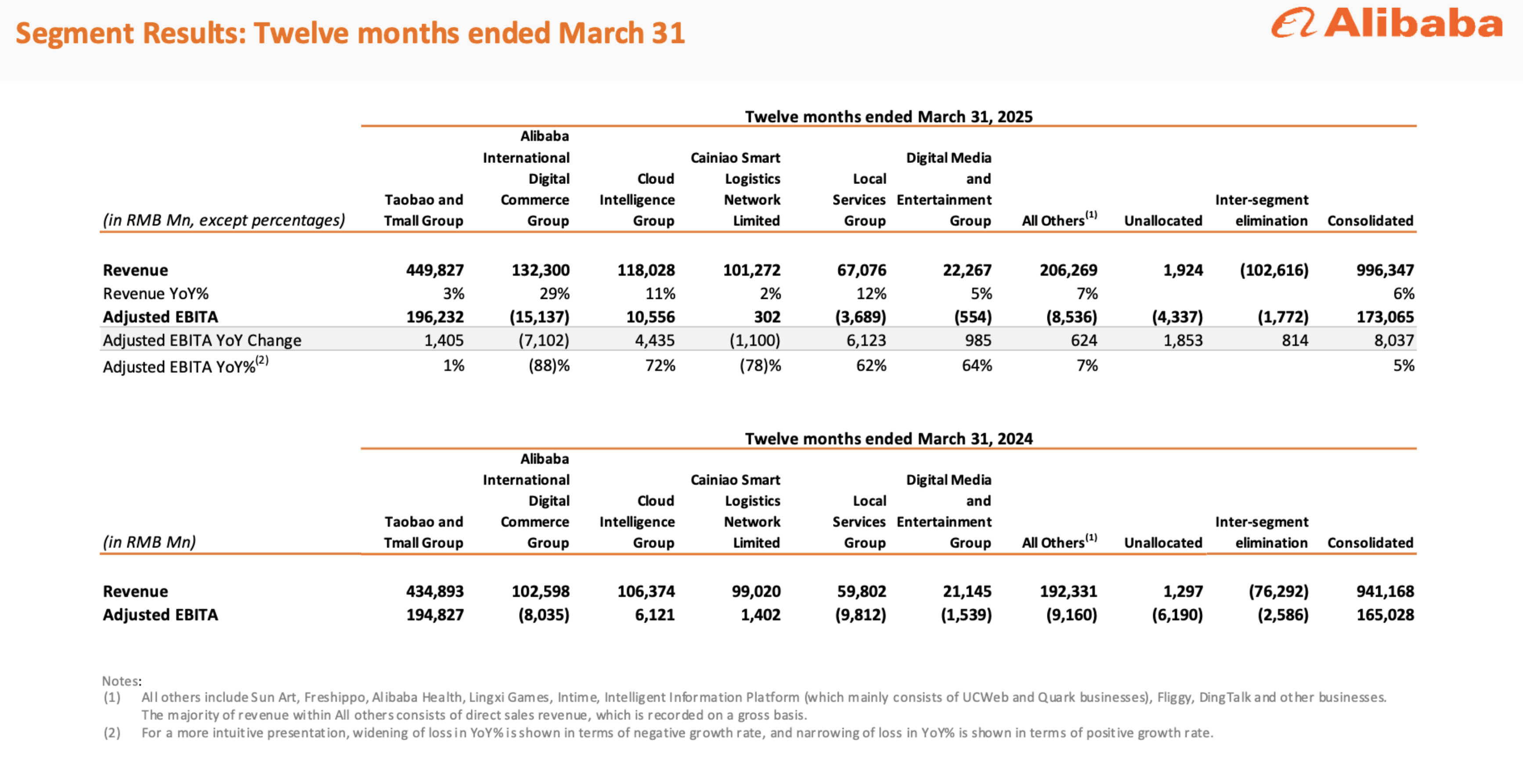

Alibaba operates primarily through three businesses. Domestic marketplaces (Taobao and Tmall), Cloud Intelligence, and AIDC (International Digital Commerce). But when you look closely at the bottom line, only one part of the business generates meaningful profit.

You can see below from the 2024 fiscal year that Taobao and Tmall constitute about 95% of Alibaba’s total profit, Cloud contributes around 5%, and all other segments together lose money. In this scenario, I consider Alibaba’s profit to be almost entirely driven by its core domestic business.

Adjusted EBITA (in millions of RMB):

Taobao & Tmall: +196,232.

International: –15,137.

Cloud: +10,556.

All Others: –18,566.

Taobao and Tmall generate over $1.1 trillion in GMV and this year, their EBITA margin declined by around 21%. I don’t like to rely too much on that metric, but directionally it tells us something important.

Is this temporary?

In my view, it’s primarily due to intense competition. I expect margins to stabilize at lower levels rather than recover meaningfully. If they do bounce back, that would surprise me. Lower margins simply mean lower profits, and since Taobao/Tmall are the profit engine for the entire group, that’s a concern.

International commerce isn’t profitable yet, and even if it becomes profitable, margins won’t be anywhere near the domestic core. The cloud business, meanwhile, runs on thin margins and will require significant investment going forward.

With the current setup, I expect free cash flow to decline meaningfully while CapEx increases. That means investors are now paying higher multiples for lower growth compared to when I first wrote about Alibaba.

Growth at the Cost of Margins

Taobao and Tmall are still growing GMV, but at the cost of profitability. International commerce is growing fast in percentage terms, but it’s not yet breakeven, and running an international e-commerce business is capital intensive.

You need to invest in warehouses, logistics, and local merchant support. Take Trendyol as an example, it’s been growing fast in Turkey but now faces fresh competition after Hepsiburada was acquired by Joint Stock Company Kaspi.kz (KSPI) in January of this year, the second-largest e-commerce platform after Trendyol by GMV. Kaspi will likely start by investing in logistics and delivery and then move toward fintech integration. They have the operational strength to back it.

Alibaba’s Lazada and AliExpress platforms face similar challenges, requiring constant investment to stay competitive. All of these examples show that international growth comes at the cost of margins, with constant investment and new players entering markets all the time — PDD’s Temu, Kaspi, Sea Limited’s (SE) Shopee, and others. These are investment-heavy bets that take time before they start paying off.

Cloud

Cloud remains the most interesting part of Alibaba to watch. It’s back to double-digit growth, which is good to see, but management expects to invest around $50 billion over the next four years.

I don’t believe Alibaba will generate that much free cash flow before 2028, meaning this will likely be financed through debt or convertible notes. The cost may be low, but it still dilutes value in the short term.

It’s Fairly Valued

Alibaba’s core e-commerce business, Taobao and Tmall, generate about $65 billion in revenue and roughly $27 billion in profit. I value it at around $270 billion using a 10× earnings multiple, given the intense competition and declining margins.

The international e-commerce segment is growing quickly but is not yet profitable. With around $75 billion in GMV and a 3% take rate, I value it at about $25 billion, bringing the total e-commerce value to $295 billion.

Alibaba Cloud remains the market leader in China and across Asia-Pacific. Assuming regional cloud market grows to $500 billion and Alibaba captures 20%, that could mean $100 billion in revenue and $25 billion in profit. I estimate this business to be worth around $150 billion today. Adding about $25 billion for Ant (Alibaba’s fintech affiliate), logistics, and other smaller businesses brings the total to $470 billion. After applying a 30% margin of safety, that comes down to $329 billion, and with $70 billion in adjusted net cash and investments, my fair value estimate is roughly $399 billion.

So, if the current market cap is around $400 billion, Alibaba looks fairly valued, trading around intrinsic value. To have a 30% margin of safety, I’d want the market cap closer to $280 billion before calling it a Buy.

Not Cheap!

At today’s nearly $400 billion market cap, Alibaba generated about $10 billion in free cash flow in FY2024 (ending March 2025), meaning investors are paying roughly 40× FCF.

I get the excitement among investors around AI, cloud, and Alibaba’s profitable core business; however, considering the growing competition, declining margin trends, and rising capex requirements, investors now face a real risk of overpaying for future growth in a business that’s growing single digits.

If you look at the long-term trend, operating margins have fallen from around 30% to roughly 15% today. With the company planning large CapEx and heavy cloud investment, I don’t see that trend reversing soon.