Adobe: The Stock Is Cheap, But the Business Is Changing

Adobe stock looks cheap after a 70% decline, but the real question is whether AI, Firefly, Creative Cloud and Acrobat can protect free cash flow and long-term pricing power.

At its peak in November 2021, Adobe was worth about $328 billion in the market.

By mid-May 2026, Adobe was closer to $100 billion.

So roughly $225-$230 billion of market value has disappeared. That is about a 70% decline from the peak.

Back then, Adobe was treated like one of the cleanest software compounders in the world: high recurring revenue, high gross margin, strong free cash flow, and deep creative workflows. Today, the question is whether generative AI lowers the value of basic creation, shifts workflows toward other AI platforms, raises costs, and makes it harder for Adobe to turn usage into paid recurring revenue.

Adobe is still a very profitable software business with a strong five-year record, but AI is attacking the exact area where Adobe has historically made money.

What Adobe Really Is

The company makes money mainly through subscriptions. In fiscal 2025, Adobe generated $23.8 billion of revenue. Of that, $22.9 billion was subscription revenue. It is collecting recurring revenue from tools and platforms that people and companies use repeatedly.

Digital Media is the main business. In FY2025, it produced $17.65 billion of revenue, grew 11%, and generated $16.81 billion of gross profit. That is where Creative Cloud, Document Cloud, Acrobat, Photoshop, Illustrator, Premiere, Express, Firefly and the related tools sit.

Digital Experience is smaller, but still meaningful. It produced $5.86 billion of revenue, grew 9%, and generated $4.24 billion of gross profit. This is where Experience Cloud, Adobe Experience Platform, GenStudio, analytics, customer data, marketing workflows, commerce, Workfront and enterprise experience software sit.

Publishing and Advertising is no longer central to the thesis. It produced only $0.26 billion of revenue in FY2025, declined 7%, and generated $0.17 billion of gross profit.

The core software economics are still very strong. Digital Media produced gross profit equal to 95% of revenue. That does not mean 95% drops to the bottom line, because Adobe still spends heavily on R&D, sales, marketing and administration. But it does show why the business has been such a strong cash generator.

The AI debate is about protecting this high-quality base while building new revenue streams. If AI helps Adobe sell more Creative Cloud, Acrobat, Firefly, Express, GenStudio and Experience Platform products, the business can keep compounding. If AI forces Adobe to give away more value for free or accept lower pricing, the historical economics become less useful.

In fiscal 2026, Adobe changed the reporting structure and now has one operating and reportable segment. From an investor perspective, that gives less visibility, although Adobe still gives customer group subscription revenue.

For the full fiscal year 2025, Creative & Marketing Professionals produced $16.30 billion of subscription revenue and grew 11%. Business Professionals & Consumers produced $6.50 billion and grew 15%. Together, Digital Media and Digital Experience subscription revenue was $22.80 billion, up 12%.

The same pattern continued in Q1 FY2026. Creative & Marketing Professionals produced $4.39 billion of subscription revenue and grew 12%. Business Professionals & Consumers produced $1.78 billion and grew 16%. Total Customer Group subscription revenue was $6.17 billion, up 13%.

Creative & Marketing Professionals is still the larger revenue base. Business Professionals & Consumers is smaller, but it was the faster-growing customer group in FY2025 and again in Q1 FY2026.

That helps explain the strategy. Adobe is not just a creative professional company anymore. It wants to serve professional creators, marketers, office workers, consumers, students, small businesses and large enterprises.

If AI makes creation easier, more people can create. A student can make a presentation. A small business owner can make an advert. A marketer can generate campaign variations. A large company can automate thousands of content assets. A normal office worker can turn a PDF into a summary, deck, infographic or audio file.

The Products

1. Creative Cloud

Creative Cloud is still the heart of the company. It includes products like Photoshop, Illustrator, Premiere Pro, After Effects, Lightroom and InDesign. These are the tools many professional creators, designers, video editors, photographers and creative teams already know.

Adobe said FY2025 Digital Media subscription growth was driven by strength in Creative Cloud Pro, other flagship apps and Acrobat. In Q1 FY2026, management again said Creative Cloud growth was driven by the CC Pro offering.

This is the core cash engine. It is not only because the apps are good. It is because the products are learned, shared, used inside teams, connected to files, tied to creative habits, and used in professional workflows. That is harder to replace than a single image-generation tool.

The risk is that AI makes some parts of creation easier and cheaper. If that only helps Adobe users do more inside Creative Cloud, it is positive. If it makes customers question why they need the full paid workflow, it becomes a problem.

2. Acrobat, Acrobat Studio And Express

Acrobat is the document side of Adobe. It lets users read, edit, sign, create and work with PDFs. That may sound less exciting than AI image generation, but documents are a huge daily workflow. Businesses do not stop using PDFs because a new AI tool appears.

Adobe is now trying to turn Acrobat from a document tool into a broader productivity and creation platform. Acrobat Studio brings together Acrobat, Express and AI agents. Acrobat AI Assistant can summarise documents, answer questions, cite sources and help create formatted content.

That group produced $6.50 billion of subscription revenue in FY2025, up 15%, and $1.78 billion in Q1 FY2026, up 16%.

The latest product signals are good. Acrobat + Express MAU grew about 20% year over year in Q1. Acrobat AI Assistant ARR grew about 3x. Management also said Acrobat Studio saw strong upgrades as part of enterprise licence renewals.

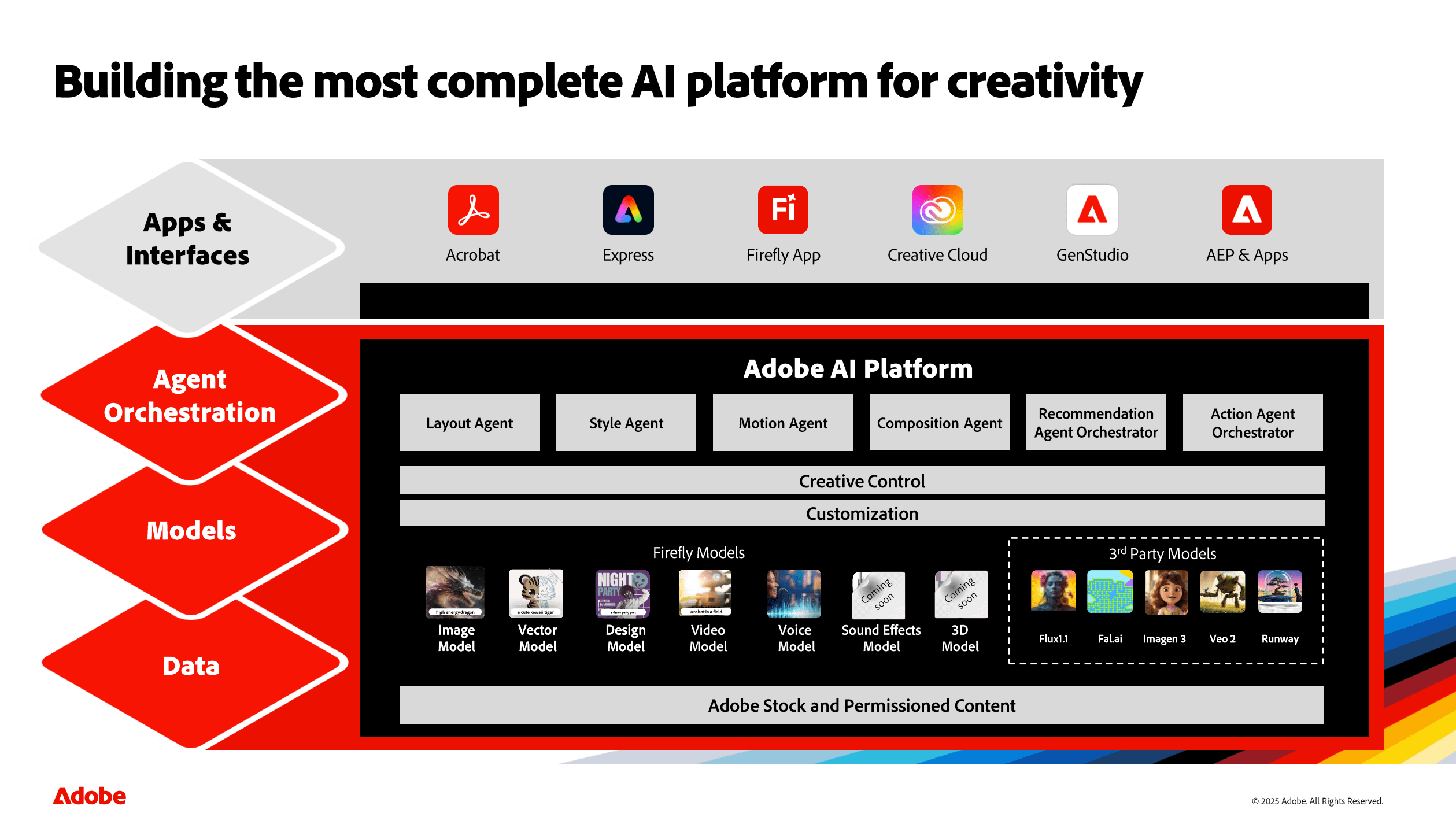

3. Firefly

Firefly is Adobe’s generative AI product family. It is not one small feature. It includes Adobe’s own Firefly models, the Firefly app, Firefly credit packs, Firefly Enterprise, Firefly Services and Firefly Foundry.

Firefly helps users generate and edit creative content with AI. It is used across images, design, video and other creative workflows. Adobe’s own filings describe Firefly models as commercially safe and trained on licensed content and public domain assets. That is important for enterprise customers because companies care about rights, brand safety and legal risk.

Firefly is Adobe’s clearest AI revenue signal. Adobe is not only adding AI features to defend the old business. It is trying to charge for AI through the Firefly app, credit packs and enterprise products.

Firefly ending ARR exceeded $250 million in Q1 FY2026. Total Adobe ARR was $26.06 billion. Firefly is real, but still small. It proves Adobe can charge for AI, but it does not yet prove that AI can move the whole company.

4. Adobe Stock

Stock is the warning sign.

Adobe Stock gives customers access to licensed creative assets. Historically, that was a useful model. If you needed an image, video or other asset, you could license it rather than create it from scratch.

Generative AI changes that behaviour. If a user can generate a good enough asset, the old standalone Stock model weakens.

Management said the traditional standalone Stock business declined more than expected in Q1 FY2026 and that the shift is happening faster than planned. Adobe’s strategy is to give customers a choice between stock and generative AI for creative and marketing workflows.

I like that they are being direct about the issue. But I would not ignore it. Stock may be small compared with the whole company, but it is one of the cleanest examples of AI replacing an older content model.

5. GenStudio And Adobe Experience Platform

GenStudio and Adobe Experience Platform sit more on the enterprise marketing side.

Adobe describes GenStudio as a content supply chain solution. In plain English, it helps large companies plan, create, produce, activate, deliver, manage and measure marketing content. It connects tools like Adobe Experience Manager Assets, Workfront, Firefly Services and GenStudio for Performance Marketing.

Adobe Experience Platform is the customer data and orchestration layer. It helps companies collect and activate customer data across channels, then use that data for personalization, journey management, analytics and marketing execution.

This is not as easy to understand as Photoshop or Acrobat, but it may be very important. Large companies need more content, more personalization, more measurement and more control. If AI increases content volume, enterprises need systems to manage that content without losing brand control.

Management said GenStudio and AEP & Apps ending ARR each grew over 30% year over year in Q1 FY2026. It also said the number of customers with ARR over $10 million grew more than 20%.

Enterprise demand is still there. The issue is whether it becomes a larger profit engine over time. Digital Experience had $5.86 billion of revenue in FY2025 and $4.24 billion of gross profit. That is a good business, but the gross profit rate is lower than Digital Media. It needs scale and execution.

6. Workfront, Frame.io, Substance 3D And Other Workflow Products

Adobe also owns products that are less visible to casual investors but matter inside workflows.

Workfront is work management for teams. Frame.io supports video collaboration and review. Substance 3D is used for 3D content creation. Adobe Commerce, Marketo Engage, Journey Optimizer, Analytics, Customer Journey Analytics and Real-Time CDP all sit inside the enterprise experience stack.

Adobe does not disclose each product’s revenue or profit. These products matter because they make the platform harder to replace. The more Adobe connects creation, collaboration, data and activation, the stronger the workflow argument becomes.

The main enterprise question is whether GenStudio, AEP and Experience Cloud can become a larger part of the cash flow story.

The Five-Year Record

Adobe’s recent numbers still show a business that has grown. Revenue went from $15.8 billion in fiscal 2021 to $23.8 billion in fiscal 2025.

Revenue was $15.8 billion in FY2021, $17.6 billion in FY2022, $19.4 billion in FY2023, $21.5 billion in FY2024, and $23.8 billion in FY2025.

Operating cash flow also moved higher over time. It was about $7.2 billion in FY2021, $7.8 billion in FY2022, $7.3 billion in FY2023, $8.1 billion in FY2024, and $10.0 billion in FY2025.

That is roughly 11% annual revenue growth over four years. The cash flow record is also strong, although not perfectly smooth. Fiscal 2023 and fiscal 2024 were not as clean as fiscal 2025. But by fiscal 2025, Adobe produced more than $10 billion of operating cash flow.

Capex is very low for a company of this size. In fiscal 2025, Adobe spent only $179 million on property and equipment. That leaves roughly $9.85 billion of free cash flow if I use operating cash flow minus capex.

For an owner, the point is that Adobe does not need a lot of physical capital to keep the business running. The company spends heavily on people, R&D, sales, marketing, cloud infrastructure and products, but the cash economics are still very good.

In FY2025, GAAP operating income was $8.7 billion. Non-GAAP operating income was about $11.0 billion. In Q1 FY2026, GAAP operating income was $2.4 billion and non-GAAP operating income was $3.0 billion. Q1 non-GAAP operating income was 47.4% of revenue.

The Business Engine

First, the tools are deeply used. Creative professionals learn Photoshop, Illustrator, Premiere, After Effects, InDesign and Lightroom. Companies build teams, templates, libraries, brand processes and production workflows around these products. In documents, Acrobat and PDF have decades of habit behind them. In marketing, Adobe is used inside large companies that need analytics, content management, customer data, campaign management and workflow control.

Second, the business is recurring. Customers do not buy a new Photoshop box every few years. They subscribe. Enterprises renew. Users upgrade. Teams add seats. Customers move between plans and products.

Third, Adobe is trying to attach AI to workflows customers already use. A prompt-based AI image tool may be useful, but it is not the same thing as a full production workflow. A brand team does not only need an image. It needs rights, consistency, editing, approvals, brand safety, collaboration, formatting, storage, delivery and measurement.

Q1 FY2026

Q1 FY2026 had strong operating numbers and early AI signals. Total revenue was $6.40 billion, up 12%. Subscription revenue was $6.20 billion, up 13%. Total Adobe ARR was $26.06 billion, up 10.9%. Operating cash flow was $2.96 billion, and Adobe repurchased about 8.1 million shares in the quarter.

The usage numbers were also strong. Adobe surpassed 850 million monthly active users across Acrobat, Creative Cloud, Express and Firefly, up 17%. Creative freemium MAU crossed 80 million, up more than 50%. Acrobat + Express MAU grew about 20%.

The AI monetization signs are still early, but they are not zero. AI-first application ARR more than tripled year over year. Firefly ending ARR, across Firefly App, Firefly credit packs and Firefly Enterprise, exceeded $250 million. AEP & Apps and GenStudio ending ARR each grew more than 30%, and total customers with ARR over $10 million grew more than 20%.

The latest quarter shows why the AI debate is difficult. User growth is moving first. MAU, freemium usage, credit consumption, Express, Firefly and Acrobat AI Assistant are all moving in the right direction.

The revenue proof is earlier. Firefly ending ARR is above $250 million, while total Adobe ARR is about $26 billion. Adobe needs more than usage. It needs paid conversion and durable economics.

The Stock Business Is A Warning

Management said the traditional standalone Stock business declined more than expected in Q1, and that the shift is happening faster than planned.

I would not make too much of this by itself. Stock is not the whole Adobe business. But it is still useful evidence because it shows where AI can substitute for an older content model.

If a customer can generate an image instead of buying a stock asset, part of the old model weakens. Adobe knows this and is trying to give customers a choice between stock and generative AI. That may be the right strategy. But it still shows the risk.

The bigger question is whether Stock is the small part that gets disrupted, or the early example of a wider change in creative workflows.

If the disruption stays around standalone Stock and Adobe replaces it with Firefly, credit packs, Firefly Enterprise and GenStudio, the bear case weakens.

If the same pressure spreads into Creative Cloud pricing, upgrade behaviour or enterprise renewals, the bear case gets much stronger.

The Bull Case

The bull case is not that AI does not matter. The bull case is that AI makes Adobe more useful.

A person who never learned professional software may start with Express, Firefly or Acrobat AI Assistant. Some of those users may never pay. But some may. A student may become a creator. A small business may become a paid team. An enterprise may use Firefly Services to automate content production. A brand may use GenStudio to generate, review, govern and activate assets across channels.

Adobe’s advantage is that it can connect creation with editing, documents, brand control, customer data, marketing workflows and enterprise governance.

A generic AI model can create something impressive. But large companies need more than impressive. They need content that fits brand rules, legal requirements, approval processes and campaign systems. They need to know where the asset came from. They need controls. They need reliability. They need people across teams to work with the same files and the same standards.

Adobe’s old strengths may become useful again when enterprises need governed content, approvals and measurement, not only a generated asset.

The company has products across the whole chain:

Photoshop, Illustrator, Premiere, After Effects, Lightroom and InDesign for professional creative work.

Acrobat, PDF, Acrobat Studio and AI Assistant for document work.

Express and Firefly for lighter creation and new users.

Firefly Services and Firefly Foundry for enterprise AI content production and custom models.

Frame.io and Workfront for collaboration and production workflow.

Adobe Experience Manager, Adobe Experience Platform, Analytics, Journey Optimizer, Commerce, GenStudio and related products for customer experience and marketing workflows.

I would not describe Adobe as only a tool company. The stronger version is that Adobe owns important parts of the content and marketing workflow.

The Bear Case

The bear case is also real. It is not that Adobe disappears. It is that the business becomes a slower-growing, more expensive-to-run software company with less pricing power. The risk shows up in seven places.

First, AI may reduce the value of basic creation. If a user can create a good enough image, video, presentation or design in a chatbot or a cheap AI app, Adobe has to prove why the paid workflow is still worth it. Professionals may stay. Enterprises may stay. But entry-level and casual users may be harder to monetize.

Second, Adobe may get usage without economics. Management is clear that freemium is part of the strategy. Creative freemium MAU grew more than 50%, which sounds excellent. But management also said this approach has a near-term impact on ARR. That is the right trade-off if free users convert later. It is the wrong trade-off if Adobe trains users to expect more creation for free.

Third, AI may shift distribution away from Adobe-owned surfaces. Adobe is integrating with ChatGPT and other AI platforms. That can bring reach. But it can also make Adobe more dependent on third-party platforms. If users start creation inside OpenAI, Google, Microsoft, Anthropic or another assistant, Adobe needs to make sure it still owns enough of the workflow and economics.

Fourth, AI can raise costs. Adobe’s own 10-Q says developing, testing and deploying AI systems can increase compute costs and that adoption and monetization pathways are uncertain. That is plain enough. AI can make the product better, but if the company must spend more on infrastructure, models, datasets, compliance and indemnity, the cash flow argument becomes more complicated.

Fifth, AI brings legal, IP and regulatory risk. Adobe’s filings discuss AI regulation, third-party model risk, training data, IP claims, privacy claims and reputation risk. Adobe sells trust to enterprises. If customers are buying Adobe partly because it is commercially safer, Adobe has to keep that trust.

Sixth, reporting is now less detailed. Adobe combined its old segments into one operating and reportable segment in Q1 FY2026. Management says this reflects unified selling and integrated product innovation. That may be true. But from an investor view, less segment detail makes it harder to see exactly what is working and what is weakening.

Seventh, there is a CEO transition. Shantanu Narayen has led Adobe for a long time.

What The Numbers Say Today

Q1 FY2026 revenue grew 12%. Customer group subscription revenue grew 13%. Operating cash flow was a Q1 record at $2.96 billion. The company had $6.89 billion of cash and short-term investments exiting the quarter. Non-GAAP operating income was 47.4% of revenue.

For FY2026, management reaffirmed revenue of $25.90 billion to $26.10 billion. It expects Business Professionals & Consumers subscription revenue of $7.35 billion to $7.40 billion, Creative & Marketing Professionals subscription revenue of $17.75 billion to $17.90 billion, Total Adobe ending ARR growth of 10.2%, and non-GAAP operating margin around 45%.

If Adobe can grow revenue around 9-10%, keep non-GAAP profitability around the mid-40s as a percentage of sales, and keep producing close to $10 billion or more of free cash flow, the market does not need a perfect AI story.

By mid-May 2026, Adobe was roughly a $95-$100 billion company. Against FY2025 free cash flow of about $9.85 billion, that is around 10x owner earnings. Against my rough FY2026 cash generation base of about $10.5 billion, it is closer to 9-10x. The stock is no longer priced like a perfect software story.

Valuation

Before I put numbers into a DCF, I want to think about the stock like I am buying the whole business.

That is the Buffett way of thinking I find useful. It is a piece of a business. The market cap is what the market is asking me to pay for the whole company today. The value of the business is the present value of the cash it can generate for owners over its life.

So the question is not only whether Adobe trades at 9x, 10x or 12x free cash flow.

The question is whether the whole business is worth more than the market cap today, after discounting the future cash Adobe can realistically produce.

In FY2025, Adobe produced $10.03 billion of operating cash flow and spent $179 million on property and equipment. That gives me about $9.85 billion of free cash flow.

For FY2026, management is guiding to $25.90-$26.10 billion of revenue, 10.2% Total Adobe ending ARR growth, and non-GAAP operating margin around 45%. Using the midpoint of the revenue guide and a low-40s free cash flow margin, my working free cash flow base is about $10.5 billion.

If AI weakens pricing power and Adobe becomes a no-growth cash flow business, I would use a low terminal multiple, maybe 8-10x free cash flow. If Adobe stays durable but grows more slowly, 12-15x free cash flow is more reasonable. If AI expands the workflow and Adobe keeps strong growth and high margins, then 18x can be argued. I would be careful using anything above that unless the evidence becomes much clearer.

In the stress case, I assume free cash flow declines 2% a year, use an 11% discount rate, and apply an 8x terminal multiple to year-10 FCF. That gives about $81 billion of equity value, or roughly $201 per share.

In the no-growth case, I assume cash generation stays flat and apply the same 8x terminal multiple. That gives about $98 billion of equity value, or roughly $241 per share.

In the bear-but-still-durable case, I assume free cash flow grows 3% a year and the terminal multiple is 10x. That gives about $130 billion of equity value, or roughly $320 per share.

In the base case, I assume owner cash grows 6% a year and Adobe still deserves a 15x terminal multiple. That gives about $196 billion of equity value, or roughly $484 per share.

In the bull case, I assume free cash flow grows 9% a year and the terminal multiple is 18x. That gives about $273 billion of equity value, or roughly $676 per share.

I do not treat this as a target price. I use it to see what the current price already assumes.

At around a $95-$100 billion market cap, the market is close to my no-growth case. That means investors are not paying much for future growth today.

If the bear case is right and AI slowly reduces Adobe’s pricing power, raises costs, weakens Creative Cloud monetization, and turns more usage into lower-quality revenue, then the stress case matters. A low multiple will not protect me if the cash flow base starts going backwards.

But if Adobe can keep producing more than $10 billion of free cash flow, grow that cash flow even in the low single digits, and still deserve a 10-12x terminal free cash flow multiple, the current valuation looks too cheap.

Adobe has to show that AI is not only defending the old business. It has to become a paid workflow layer across Creative Cloud, Acrobat, Express, Firefly, GenStudio and Experience Cloud. That is what would support the base or bull cases.

In FY2025, the company repurchased about 30.8 million shares and spent $11.3 billion on common stock repurchases. In Q1 FY2026, it repurchased another 8.1 million shares for about $2.5 billion. The March 2024 authorization was for up to $25 billion, and $3.89 billion remained at the end of Q1.

My Current View

The current business is strong. The five-year record is good. Adobe still produces a lot of cash. The products are deeply used. The balance sheet is fine. The buyback can help per-share value.

But the bear case is not imaginary. AI attacks the centre of the company. It changes who can create, where they create, how much they pay, what tools they need, and what platforms own the customer relationship.

Adobe has a real chance to use AI to expand the number of creators and business users. More people can create because the tools are easier. More companies need content because digital channels keep multiplying. More marketing teams need automation because manual content production cannot keep up. If Adobe keeps the workflow, trust and cash economics, AI can make the company more valuable.

The valuation is what makes the idea interesting. At around a $95-$100 billion market cap, Adobe is close to my no-growth case. My stress case was around $81 billion of equity value. Based on my valuation work, I think downside risk is more limited.

I want ARR to stay around double-digit growth while free cash flow remains strong. I want Firefly, Acrobat AI Assistant, GenStudio, AEP AI products and Firefly Enterprise to become material revenue sources, not only usage stories. I want Creative Cloud and Acrobat upgrades to show that customers will pay more because AI makes the products more valuable. I also want margins and cash conversion to hold while Adobe invests in AI.

Stock is the product-level warning sign. If standalone Stock declines but Adobe replaces it with Firefly and enterprise content automation, that is acceptable. If Stock is the first sign of broader Creative Cloud pricing pressure, the view has to change.

Enterprise retention, Creative Cloud pricing and seat behaviour are the faster signals. If customers start using AI to reduce Adobe seats rather than expand usage, the thesis changes quickly. Cost matters too. AI compute, model costs, compliance, indemnity, data and infrastructure spending cannot keep rising if cash generation starts to weaken.

Adobe is going through a major product transition at the same time as a leadership transition. That does not have to be a problem, but it is not nothing.

The question is whether AI increases Adobe’s useful role in the workflow, or slowly gives away the value of creation to cheaper tools and third-party platforms.

Not investment advice. Just my own thinking.

Well written. Might it be so that us "normal" people without insight in deep creative work cant fully grasp the true moat of Adobe? My gut says that people underestimate them. And overestimate AI. They are adapting, maybe more so then anyone.

Excellent and thorough analysis