Dear Partners,

Happy Holidays to you and your families. It is the most beautiful time of the year to be with loved ones.

As we end 2025, I want to share my learnings, experiences, and a reflection on how the year went for the portfolio.

I have been in the investing world long enough to know that the downside matters the most. If you do not respect it, hard lessons will be learned.

As a result, the first principle of my investment approach is shaped by Warren Buffett’s two rules: never lose money, and never forget rule number one.

I believe this concept is not well understood by many. These rules are the foundation of everything I do because, in investing, the downside matters more than the upside. If you lose 50% of your capital, you need a 100% gain just to recover your initial investment. That is why I focus on what can go wrong before I look at what can go right. For this reason, I view my job primarily as risk management, rather than just investing.

Performance

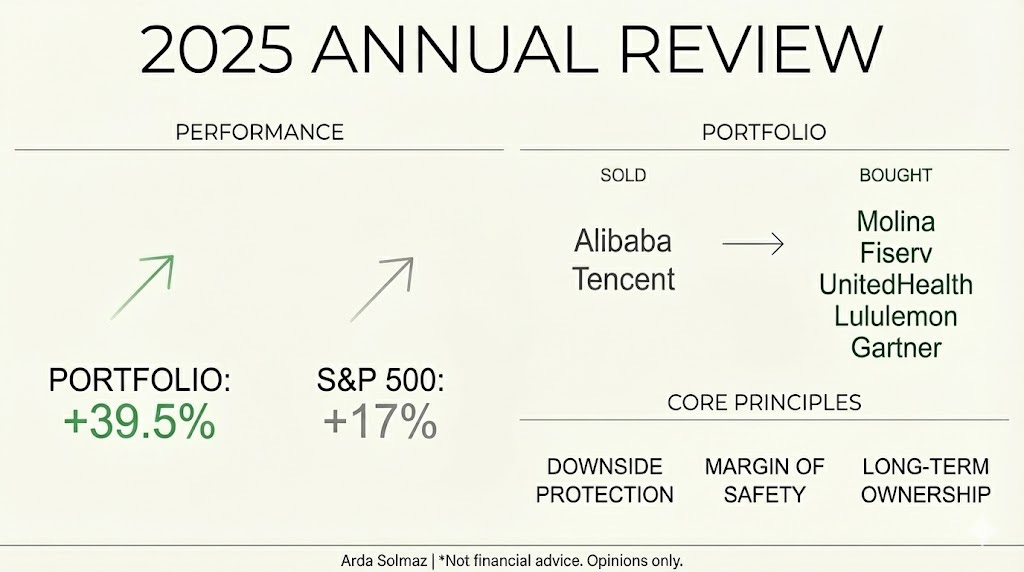

As of today, the portfolio has appreciated 39.5% in 2025. By comparison, the S&P 500 has returned 17%. This marks the third consecutive year of outperformance against the index.

Annual Returns vs. S&P 500:

2023: Portfolio +33% (Index: +21%)

2024: Portfolio +36% (Index: +23%)

2025: Portfolio +39.5% (Index: +17%)

Cumulative Return (3-Year Total):

My Portfolio: 150%

S&P 500: 75%

Portfolio Changes

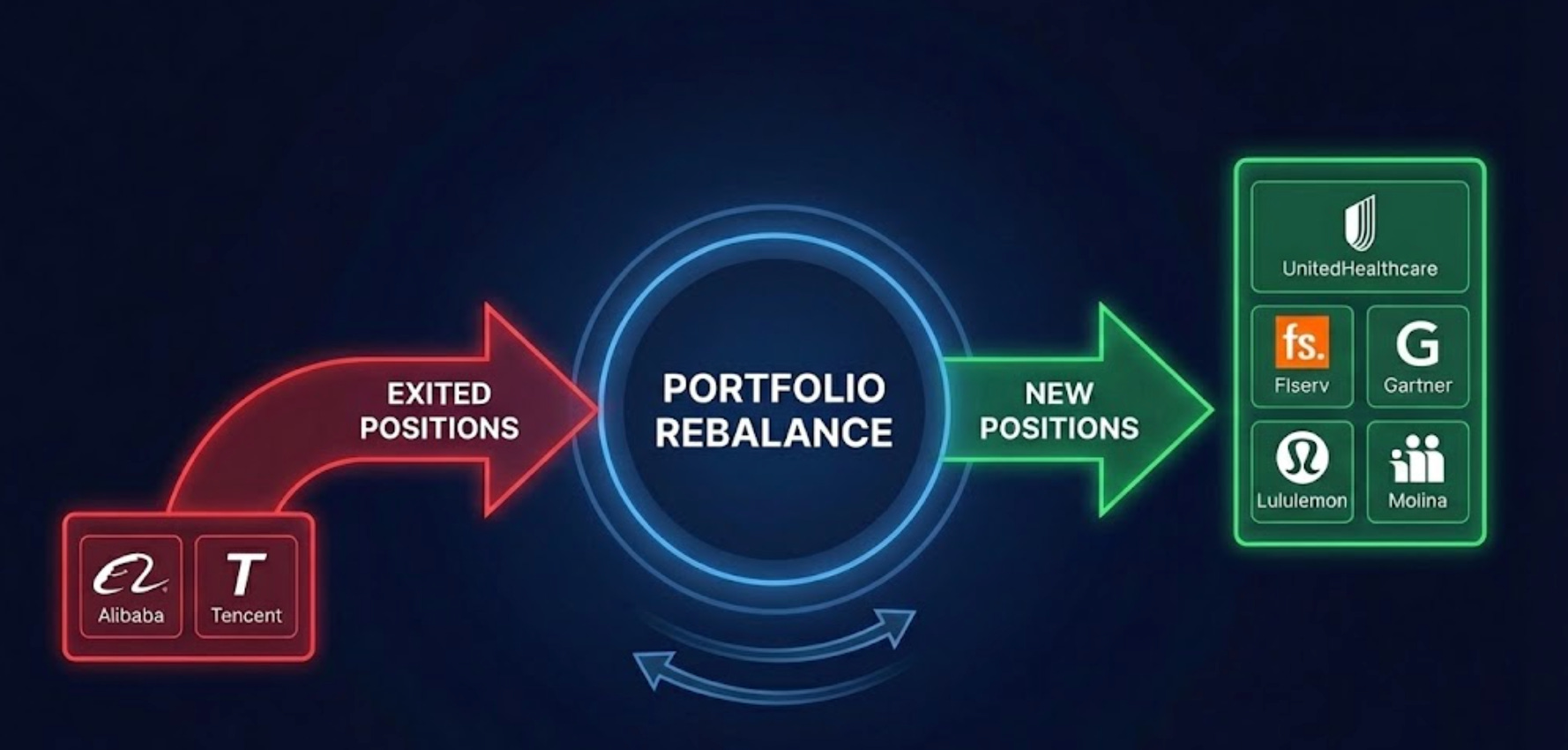

I sold my positions in Alibaba and Tencent.

Tencent is, in my opinion, the best business in China. It is one of the few companies in the world that can grow revenue while also increasing profit margins at that scale. Its ecosystem is unique and powerful. However, I read everything through English translations. I believe that to truly understand a business, you must understand the local life and culture around it. Since I lack that direct insight, I require a massive margin of safety to own Chinese stocks.

Alibaba faces a different problem. E-commerce is a tough business. Competitors like Pinduoduo and JD are fighting for market share and reducing every bit of margin. To keep their market share, Alibaba has to lower prices. As a result, their profit margins have been dropping for the last few years. They are also spending more money just to earn the same amount of revenue.

I bought Alibaba because it was very cheap; the company traded at a very low earnings multiple and had generated strong free cash flow for many years. However, the stock price has gone up about 100% since then, while free cash flow has dropped significantly, even turning negative due to high CapEx. Although they might win in cloud computing and AI, or stabilize their e-commerce margins in the long term, the setup has changed. With the price substantially higher and the business economics getting tougher, there was not enough margin of safety left to justify holding it. I decided to sell and move this capital into 4 high-conviction US-based businesses

UnitedHealth & Molina

UnitedHealth is now my largest holding. It provides massive scale and predictable earnings. Molina is different. It focuses mainly on Medicaid and operates with a very low-cost structure, which makes it highly efficient at managing government contracts.

I saw the recent drop in their share prices as a chance to buy.

Lululemon is my second-largest holding. The stock dropped earlier this year because sales growth slowed in North America. I think it is a good business. They sell premium products and earn high returns on their capital. They also have huge room to grow internationally, especially in China and Europe. We bought a premium brand for the price of an average retailer.

Gartner

In December, I initiated a position in Gartner, which is now a top-3 holding.

Gartner provides essential research and advisory services to executives. I view their service as “risk mitigation” for corporate decision-makers. Before a CTO commits significant capital to software, they require independent validation.

The stock sold off on fears that Artificial Intelligence would displace human analysts. I disagree. AI generates more data, more vendors, and more noise. In a complex environment, trusted, independent judgment becomes more scarce and valuable, not less.

Lessons from 2025

These are not brand-new lessons; they are principles I already knew, but the market has a way of reminding you of them.

1. Catching the absolute bottom is impossible. The most important reminder this year came from my decision to buy into the healthcare sector. I bought these companies after they had already fallen significantly. I believed they were cheap. However, shortly after I bought them, they went down aggressively again.

It was a reminder that you can never perfectly time the bottom. In the short term, there is no floor to a stock price, even if the valuation makes sense.

2. Temperament matters more than intellect. In investing, mistakes are part of the game. You can learn from them and improve your process, but avoiding them completely is impossible. That is why temperament and risk management are the two most important tools we have.

Prices can stay disconnected from value for a long time, even if your thesis is right. Since I never short stocks and I never use options, my only job is to own pieces of great businesses and wait. Attempting to time the market is a fool’s game; having the patience to sit through the volatility is the real skill.

Macroeconomic Outlook

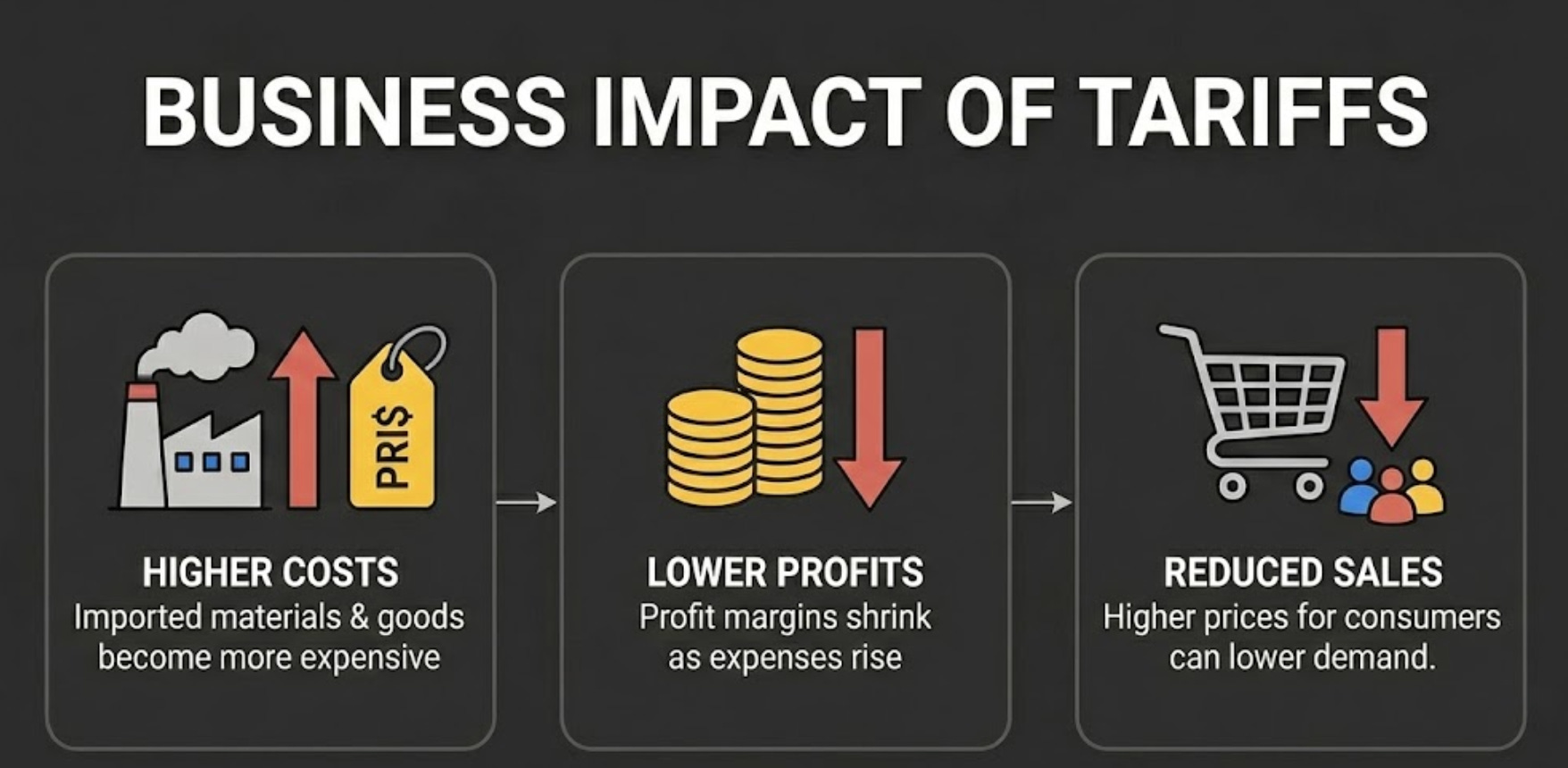

I do not make decisions based on headlines, but I stay aware of the economic environment. When new tariffs were announced, the impact was immediate, especially for companies that rely heavily on specific supply chains. Their stock prices dropped because these changes have a long-lasting impact on their profits.

Rules can change, and the world will not stay the same, so companies that hold debt can be vulnerable. That is why I prefer companies that have strong balance sheets and generate free cash flow. Currently, the S&P 500 pays you back about 2.74% a year in free cash flow. That barely keeps up with inflation. I stick to the basics: Price is what you pay. Value is what you get.

Investment Philosophy

As we look to the future, it is important to repeat the core principles

My goal is to beat the S&P 500 by ten percentage points over the long run.

I believe owning productive businesses is the best way to build wealth over time.

Owning great businesses.

Buying them for less than they are worth (Margin of Safety).

Having the right attitude.

To show the power of business ownership: $100 invested in the S&P 500 in 1957 would have grown to about $77,626 by the end of 2025. That is the power of time. My job is to avoid interrupting that growth.

I prefer a focused portfolio. As Charlie Munger said, “If a thing is not worth doing at all, it’s not worth doing well.”

I do not believe in buying our 20th best idea just to have “variety.” That just lowers our returns. Like the Walton family with Walmart, I believe in holding fewer positions where I am very confident. When the odds are in our favor, we bet big.

I realized that people are what turn a good company into a great one, whether it is the culture at Berkshire Hathaway or the drive at Amazon and Apple. To succeed, I need to find management teams that can handle change over decades, and then let them do their job.

My process is simple. I do not start with the economy. Instead, I start with the company itself. I look at the balance sheet to estimate how much money they will make in three, five, or ten years. I also check who their competitors are and if their product will last. Because the future is hard to predict, I only buy when the price is much lower than the value.

I stay away from most AI stocks right now. In the early 1900s, cars changed the world, yet hundreds of car companies went bankrupt. Similarly, in 2000, the internet changed the world, but for every Amazon, there was a Pets.com that went to zero.

I prefer to buy the winner after they have won. For example, during the internet crash, Amazon stock fell 90% and was risky. Today, it is safe and dominant. Warren Buffett followed a similar path with Apple. He did not buy it early. He bought it in 2016, after everyone already owned an iPhone. I am not looking for the next Amazon. I am looking for the businesses that have already proven they are built to last.

Thank you

Arda Solmaz

Disclaimer: I am not a financial advisor. This letter is for informational purposes only and represents my own opinions and portfolio moves. It is not investment advice. Please conduct your own due diligence.

Thank you for this article!